|

|

|

|

|

|

|

|

|

Spartan®

Semiannual Report

August 31, 2000

(Fidelity Investment logo)(registered trademark)

|

President's Message |

Ned Johnson on investing strategies |

|

|

Spartan California Municipal Income Fund |

||

|

|

Performance |

|

|

|

Fund Talk: The Manager's Overview |

|

|

|

Investment Changes |

|

|

|

Investments |

|

|

|

Financial Statements |

|

|

Spartan California Municipal Money Market Fund |

||

|

|

Performance |

|

|

|

Fund Talk: The Manager's Overview |

|

|

|

Investment Changes |

|

|

|

Investments |

|

|

|

Financial Statements |

|

|

Fidelity California Municipal Money Market Fund |

||

|

|

Performance |

|

|

|

Fund Talk: The Manager's Overview |

|

|

|

Investment Changes |

|

|

|

Investments |

|

|

|

Financial Statements |

|

|

Notes |

Notes to the Financial Statements |

|

|

|

|

|

Standard & Poor's, S&P and S&P 500 are registered service marks of The McGraw-Hill Companies, Inc. and have been licensed for use by Fidelity Distributors Corporation.

Other third party marks appearing herein are the property of their respective owners.

All other marks appearing herein are registered or unregistered trademarks or service marks of FMR Corp. or an affiliated company.

(Recycle graphic) This report is printed on recycled paper using soy-based inks.

This report and the financial statements contained herein are submitted for the general information of the shareholders of the funds. This report is not authorized for distribution to prospective investors in the funds unless preceded or accompanied by an effective prospectus.

Mutual fund shares are not deposits or obligations of, or guaranteed by, any depository institution. Shares are not insured by the FDIC, Federal Reserve Board or any other agency, and are subject to investment risks, including possible loss of principal amount invested.

Neither the funds nor Fidelity Distributors Corporation is a bank.

For more information on any Fidelity fund, including charges and expenses, call 1-800-544-6666 for a free prospectus. Read it carefully before you invest or send money.

Semiannual Report

(photo_of_Edward_C_Johnson_3d)

Dear Shareholder:

A slowing U.S. economy triggered an equity market rally during the later stages of summer, boosting most major stock indexes back into positive territory for calendar year 2000. One notable exception, however, was the Dow Jones Industrial Average, which posted a negative return during that timeframe. Fixed-income markets - particularly Treasuries - continued their yearlong trend of strong performance, as nearly every bond sector outperformed the stock market on a year-to-date basis.

While it's impossible to predict the future direction of the markets with any degree of certainty, there are certain basic principles that can help investors plan for their future needs.

The longer your investment time frame, the less likely it is that you will be affected by short-term market volatility. A 10-year investment horizon appropriate for saving for a college education, for example, enables you to weather market cycles in a long-term fund, which may have a higher risk potential, but also has a higher potential rate of return.

An intermediate-length fund could make sense if your investment horizon is two to four years, while a short-term bond fund could be the right choice if you need your money in one or two years.

If your time horizon is less than a year, you might want to consider moving some of your bond investment into a money market fund. These funds seek income and a stable share price by investing in high-quality, short-term investments. Of course, it's important to remember that an investment in a money market fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Although money market funds seek to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in these types of funds.

Finally, no matter what your time horizon or portfolio diversity, it makes good sense to follow a regular investment plan, investing a certain amount of money in a fund at the same time each month or quarter and periodically reviewing your overall portfolio. By doing so, you won't get caught up in the excitement of a rapidly rising market, nor will you buy all your shares at market highs. While this strategy - known as dollar cost averaging - won't assure a profit or protect you from a loss in a declining market, it should help you lower the average cost of your purchases. Of course, you should consider your financial ability to continue your purchases through periods of low price levels before undertaking such a strategy.

If you have questions, please call us at 1-800-544-6666, or visit our web site at www.fidelity.com. We are available 24 hours a day, seven days a week to provide you the information you need to make the investments that are right for you.

Best regards,

/s/Edward C. Johnson 3d

Edward C. Johnson 3d

Semiannual Report

Spartan California Municipal Income Fund

There are several ways to evaluate a fund's historical performance. You can look at the total percentage change in value, the average annual percentage change or the growth of a hypothetical $10,000 investment. Total return reflects the change in the value of an investment, assuming reinvestment of the fund's dividend income and capital gains (the profits earned upon the sale of securities that have grown in value). You can also look at the fund's income, as reflected in the fund's yield, to measure performance. If Fidelity had not reimbursed certain fund expenses, the past five year and past 10 year total returns would have been lower.

Cumulative Total Returns

|

Periods ended August 31, 2000 |

Past 6 |

Past 1 |

Past 5 |

Past 10 |

|

Spartan CA Municipal Income |

7.54% |

7.75% |

37.37% |

99.07% |

|

LB California Municipal Bond |

7.75% |

7.82% |

37.13% |

n/a* |

|

California Municipal Debt Funds Average |

8.00% |

6.47% |

31.08% |

94.23% |

Cumulative total returns show the fund's performance in percentage terms over a set period - in this case, six months, one year, five years or 10 years. For example, if you had invested $1,000 in a fund that had a 5% return over the past year, the value of your investment would be $1,050. You can compare the fund's returns to the performance of the Lehman Brothers California Municipal Bond Index - a market value-weighted index of California investment-grade municipal bonds with maturities of at least one year or more. To measure how the fund's performance stacked up against its peers, you can compare it to the California municipal debt funds average, which reflects the performance of mutual funds with similar objectives tracked by Lipper Inc. The past six months average represents a peer group of 113 mutual funds. These benchmarks include reinvested dividends and capital gains, if any.

Average Annual Total Returns

|

Periods ended August 31, 2000 |

|

Past 1 |

Past 5 |

Past 10 |

|

Spartan CA Municipal Income |

|

7.75% |

6.56% |

7.13% |

|

LB California Municipal Bond |

|

7.82% |

6.52% |

n/a* |

|

California Municipal Debt Funds Average |

|

6.47% |

5.54% |

6.83% |

Average annual total returns take the fund's cumulative return and show you what would have happened if the fund had performed at a constant rate each year. (Note: Lipper calculates average annual total returns by annualizing each fund's total return, then taking an arithmetic average. This may produce a different figure than that obtained by averaging the cumulative total returns and annualizing the result.)

* Not available

Semiannual Report

Spartan California Municipal Income Fund

Performance - continued

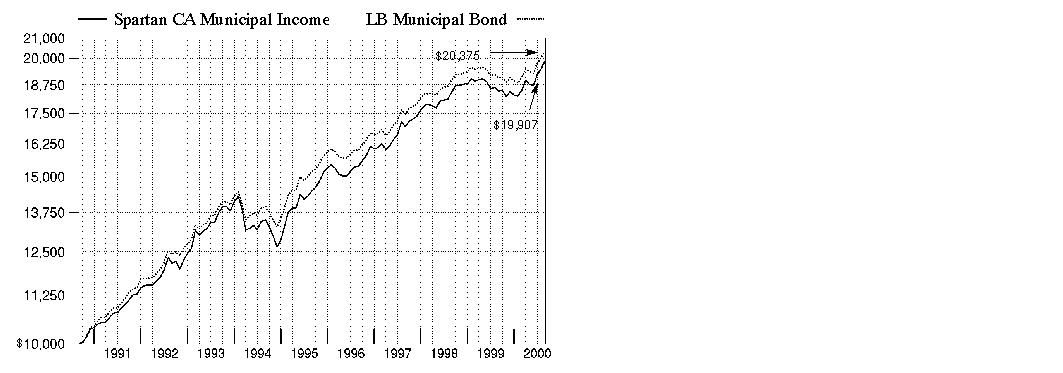

$10,000 Over 10 Years

$10,000 Over 10 Years: Let's say hypothetically that $10,000 was invested in Spartan California Municipal Income Fund on August 31, 1990. As the chart shows, by August 31, 2000, the value of the investment would have grown to $19,907 - a 99.07% increase on the initial investment. For comparison, look at how the Lehman Brothers Municipal Bond Index - a market value-weighted index of investment-grade municipal bonds with maturities of one year or more - did over the same period. With dividends and capital gains, if any, reinvested, the same $10,000 would have grown to $20,375 - a 103.75% increase.

Understanding

Performance

How a fund did yesterday is no guarantee of how it will do tomorrow. Bond prices, for example, generally move in the opposite direction of interest rates. In turn, the share price, return and yield of a fund that invests in bonds will vary. That means if you sell your shares during a market downturn, you might lose money. But if you can ride out the market's ups and downs, you may have a gain.

3Semiannual Report

Spartan California Municipal Income Fund

Performance - continued

Total Return Components

|

|

Six months ended August 31, |

Year ended |

Years ended February 28, |

Year ended |

||

|

|

2000 |

2000 |

1999 |

1998 |

1997 |

1996 |

|

Dividend returns |

2.59% |

4.46% |

4.73% |

5.23% |

5.37% |

5.86% |

|

Capital returns |

4.95% |

-6.74% |

1.27% |

4.66% |

0.79% |

5.39% |

|

Total returns |

7.54% |

-2.28% |

6.00% |

9.89% |

6.16% |

11.25% |

Total return components include both dividend returns and capital returns. A dividend return reflects the actual dividends paid by the fund. A capital return reflects both the amount paid by the fund to shareholders as capital gain distributions and changes in the fund's share price. Both returns assume the dividends or capital gains, if any, paid by the fund are reinvested.

Dividends and Yield

|

Periods ended August 31, 2000 |

Past 1 |

Past 6 |

Past 1 |

|

Dividends per share |

4.88¢ |

28.82¢ |

56.59¢ |

|

Annualized dividend rate |

4.78% |

4.87% |

4.85% |

|

30-day annualized yield |

4.55% |

- |

- |

|

30-day annualized tax-equivalent yield |

7.84% |

- |

- |

Dividends per share show the income paid by the fund for a set period. If you annualize this number, based on an average share price of $12.02 over the past one month, $11.74 over the past six months and $11.66 over the past one year, you can compare the fund's income over these three periods. The 30-day annualized yield is a standard formula for all bond funds based on the yields of the bonds in the fund, averaged over the past 30 days. This figure shows you the yield characteristics of the fund's investments at the end of the period. It also helps you compare funds from different companies on an equal basis. The tax-equivalent yield shows what you would have to earn on a taxable investment to equal the fund's tax-free yield, if you're in the 41.95% combined effective 2000 federal and state income tax bracket, but does not reflect the payment of the federal alternative minimum tax, if applicable.

Semiannual Report

Spartan California Municipal Income Fund

Market Recap

The six-month period ending August 31, 2000, was a favorable one for the municipal bond market. As the period opened, municipal bond yields were generally higher than they had been in the recent past, enticing investors who sought to protect gains in stocks when the equity markets began to recoil in mid-March. At the same time, strong U.S. economic growth and higher tax revenues led to credit rating upgrades and budget surpluses for many municipal bond issuers such as U.S. state and local governments. Thus, this solvency - in addition to higher interest rates that discouraged borrowing - curtailed new issuance, and the resulting supply/demand imbalance spurred municipal prices even higher. As the period progressed, municipal bond investors were further heartened by strong evidence that the Federal Reserve Board's series of interest-rate hikes had successfully slowed the U.S. economy, indicating that further hikes may not be necessary. That sentiment was bolstered when the Fed bypassed two opportunities to hike rates further in June and August. For the overall six-month period ending August 31, 2000, the Lehman Brothers Municipal Bond Index - an index of over 35,000 investment-grade, fixed-rate, tax-exempt bonds - returned 6.79%. In comparison, this return surpassed the gains of the Lehman Brothers Treasury, Government Bond, U.S. Agency, Mortgage-Back Securities and Credit Bond Indexes during the same time frame.

(Portfolio Manager photograph)

An interview with Christine Thompson, Portfolio Manager of Spartan California Municipal Income Fund

Q. How did the fund perform, Christine?

A. For the six-month period that ended August 31, 2000, the fund had a total return of 7.54%. To get a sense of how the fund did relative to its competitors, the California municipal debt funds average returned 8.00% for the same six-month period, according to Lipper Inc. Additionally, the Lehman Brothers California Municipal Bond Index, which tracks the types of securities in which the fund invests, returned 7.75%. For the 12-month period that ended August 31, 2000, the fund had a total return of 7.75%. In comparison, the California municipal debt funds average returned 6.47% and the Lehman Brothers California Municipal Bond Index returned 7.82%.

Q. What were some of the main forces behind the fund's performance during the past six months?

A. Anticipation that interest-rate hikes were behind us and a favorable supply/demand imbalance caused the municipal market to rally and boosted the fund's performance. Starting in the spring of 2000, investors began to anticipate that the Federal Reserve Board's yearlong campaign to stave off inflation by raising interest rates was nearing a close. That optimism was based on economic indicators that suggested economic growth might be slowing. Whether or not the Fed is finished raising interest rates will depend on the direction of the economy from here. More favorable supply and demand conditions also helped propel the municipal market. The supply of California municipals was down 24% during the first eight months of 2000, compared to the same period a year earlier. Meanwhile, the demand for municipals strengthened as bargain-hunting investors sought out their value and attractive yields. The fund's total return was the result of the appreciation of its holdings plus the income generated by them.

Semiannual Report

Spartan California Municipal Income Fund

Fund Talk: The Manager's Overview - continued

Q. Why did the fund lag its peers during the six-month period?

A. The fund generally had less interest-rate sensitivity, as measured by its somewhat shorter duration, than some of its peers for the six-month period. In keeping with Fidelity's investment approach, I didn't lengthen or shorten duration - that is, I didn't make the fund more or less interest-rate sensitive - based on where I thought interest rates would be at some point down the road. Instead, I positioned the fund to emphasize the best value opportunities based on their performance potential under a variety of possible interest-rate scenarios. I managed the fund's duration to be in line with the California municipal market as a whole, an approach that caused short-term performance to lag relative to its peers, but which has generated competitive long-term results.

Q. What factors helped the fund's performance?

A. The fund's focus on premium coupon bonds, which pay interest rates above face - or par - value, helped. One appealing aspect of premiums was that they were somewhat insulated from unfavorable tax treatment that negatively affected the prices of lower coupon bonds as rates rose. It's estimated that roughly one-quarter to one-third of all municipal bonds suffered because they were subject to that unfavorable tax treatment.

Q. What's your outlook for the municipal market?

A. As it generally does, the municipal market's performance will depend on the direction of interest rates and the supply/demand environment. While I don't forecast the direction of interest rates, my outlook for the technical aspects of supply and demand is favorable. The supply of municipals has continued to decline in response to rising interest rates because many issuers now find it too expensive to issue new or refinance old debt. As municipal bond yields rose above 6%, we saw incredibly strong demand from individual investors. To the extent that those conditions continue to prevail, municipals could do well. Another factor that could bode well for municipals is the potential for increased demand from institutional investors. If their interest in municipals re-ignites, municipals should benefit.

Semiannual Report

Spartan California Municipal Income Fund

Fund Talk: The Manager's Overview - continued

The views expressed in this report reflect those of the portfolio manager only through the end of the period of the report as stated on the cover and do not necessarily represent the views of Fidelity or any other person in the Fidelity organization. Any such views are subject to change at any time based upon market or other conditions and Fidelity disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Fidelity fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Fidelity fund.

Fund Facts

Goal: seeks a high level of current income, exempt from federal and California personal income taxes

Fund number: 091

Trading symbol: FCTFX

Start date: July 7, 1984

Size: as of August 31, 2000, more than $1.3 billion

Manager: Christine Thompson, since 1998; manager, various Fidelity and Spartan municipal income funds; joined Fidelity in 1985

3Christine Thompson on geographically diversifying the portfolio:

"One way I diversify the portfolio is to spread investments among a variety of issuers across the state, which helps protect the fund's performance against being too dependent on one sector of the economy or one area of the state. California, of course, is made up of several distinct regions, each of which tends to be driven by different economic, demographic and other factors, and each faces unique challenges looking ahead. For example, the technology- and financial services-dependent Silicon Valley/Bay Area region is currently challenged by the tech sector's volatility and the region's high cost of living. The Los Angeles area has been buoyed by the strength of the entertainment and high-tech industries. However, it is experiencing relatively high unemployment and relatively low income levels. Sacramento, where government employment plays a dominant role, is potentially one of the state's most stable regions thanks to a lower cost of living, less tight labor markets and better water availability. We'll continue to monitor each region's future challenges closely and factor them into our security selection."

Semiannual Report

Spartan California Municipal Income Fund

|

Top Five Sectors as of August 31, 2000 |

||

|

|

% of fund's |

% of fund's net assets |

|

General Obligations |

25.1 |

19.8 |

|

Transportation |

13.8 |

13.7 |

|

Electric Utilities |

11.5 |

12.3 |

|

Special Tax |

10.7 |

11.6 |

|

Escrowed/Pre-Refunded |

10.6 |

10.1 |

|

Average Years to Maturity as of August 31, 2000 |

||

|

|

|

6 months ago |

|

Years |

14.5 |

14.6 |

|

Average years to maturity is based on the average time remaining until principal payments are expected from each of the fund's bonds, weighted by dollar amount. |

|

Duration as of August 31, 2000 |

||

|

|

|

6 months ago |

|

Years |

6.9 |

7.3 |

|

Duration shows how much a bond fund's price fluctuates with changes in comparable interest rates. |

|

Quality Diversification (Moody's Ratings) |

As of August 31, 2000 As of February 29, 2000

|

Where Moody's ratings are not available, we have used S&P ® ratings. Amounts shown are as a percentage of the fund's investments. |

Semiannual Report

Spartan California Municipal Income Fund

(Unaudited)

Showing Percentage of Net Assets

|

Municipal Bonds - 96.6% |

|||||

|

Moody's Ratings (unaudited) (a) |

Principal Amount (000s) |

Value (Note 1) (000s) |

|||

|

California - 92.3% |

|||||

|

Alameda Corridor Trans. Auth. Rev. Sr. Lien Series A: |

|

|

|

|

|

|

4.75% 10/1/25 (MBIA Insured) |

Aaa |

|

$ 5,000 |

$ 4,499 |

|

|

5.25% 10/1/21 (MBIA Insured) |

Aaa |

|

7,475 |

7,381 |

|

|

Alameda County Ctfs. of Prtn Rfdg. (Santa Rita Jail Proj.) 5.7% 12/1/14 (MBIA Insured) |

Aaa |

|

2,000 |

2,089 |

|

|

Buena Park Cmnty. Redev. Agcy. Tax Allocation Rfdg. (Central Bus. District Proj.) Series A, 7.1% 9/1/14 |

BBB+ |

|

3,500 |

3,708 |

|

|

Burbank Redev. Agy. Rfdg.: |

|

|

|

|

|

|

(City Ctr. Redev. Proj.) Series A, 5% 12/1/15 (FSA Insured) |

Aaa |

|

4,000 |

4,008 |

|

|

(Golden State Redev. Proj.) Series A, |

Baa1 |

|

4,655 |

4,897 |

|

|

Cabrillo Unified School District (Cap. Appreciation) Series A: |

|

|

|

|

|

|

0% 8/1/10 (AMBAC Insured) |

Aaa |

|

2,150 |

1,364 |

|

|

0% 8/1/12 (AMBAC Insured) |

Aaa |

|

2,800 |

1,577 |

|

|

California Dept. of Wtr. Resources Central Valley Proj. Rev. (Wtr. Sys. Proj.): |

|

|

|

|

|

|

Series J1, 7% 12/1/12 |

Aa2 |

|

1,000 |

1,231 |

|

|

Series S, 5% 12/1/19 |

Aa2 |

|

3,160 |

3,080 |

|

|

California Edl. Facilities Auth. Rev.: |

|

|

|

|

|

|

(California Student Ln. Prog.) Series A, 6% 3/1/16 (MBIA Insured) (c) |

Aaa |

|

4,900 |

5,009 |

|

|

(Cap. Appreciation) (Loyola Marymount Proj.) 0% 10/1/07 (MBIA Insured) |

Aaa |

|

3,545 |

2,598 |

|

|

(Pepperdine Univ. Proj.): |

|

|

|

|

|

|

Series A: |

|

|

|

|

|

|

5% 11/1/18 |

A1 |

|

1,770 |

1,714 |

|

|

5% 11/1/29 |

A1 |

|

2,500 |

2,313 |

|

|

5.75% 9/15/30 |

A1 |

|

10,000 |

10,209 |

|

|

(Pooled College & Univ. Proj.) Series A, 6.125% 6/1/30 |

A2 |

|

3,435 |

3,592 |

|

|

(Scripps College Proj.) 5.125% 2/1/30 |

A1 |

|

6,000 |

5,666 |

|

|

(Stanford Univ. Proj.) Series N, 5.2% 12/1/27 |

Aaa |

|

20,000 |

19,490 |

|

|

Rfdg.: |

|

|

|

|

|

|

(Chapman Univ. Proj.) 5.375% 10/1/16 (AMBAC Insured) |

AAA |

|

2,000 |

2,039 |

|

|

(Claremont McKenna College Proj.): |

|

|

|

|

|

|

5% 11/1/29 |

Aa1 |

|

5,000 |

4,653 |

|

|

5.1% 11/1/17 |

Aa1 |

|

1,000 |

1,000 |

|

|

Municipal Bonds - continued |

|||||

|

Moody's Ratings (unaudited) (a) |

Principal Amount (000s) |

Value (Note 1) (000s) |

|||

|

California - continued |

|||||

|

California Edl. Facilities Auth. Rev.: - continued |

|

|

|

|

|

|

Rfdg.: |

|

|

|

|

|

|

(Santa Clara Univ. Proj.): |

|

|

|

|

|

|

5.25% 9/1/16 (AMBAC Insured) |

Aaa |

|

$ 1,650 |

$ 1,710 |

|

|

5.25% 9/1/17 (AMBAC Insured) |

Aaa |

|

1,000 |

1,024 |

|

|

5.25% 9/1/26 |

A1 |

|

7,910 |

7,757 |

|

|

(Stanford Univ. Proj.) Series O, |

Aaa |

|

8,000 |

7,674 |

|

|

(Univ. of Southern California Proj.): |

|

|

|

|

|

|

Series A, 5.7% 10/1/15 |

Aa2 |

|

5,675 |

5,997 |

|

|

Series C, 5.125% 10/1/28 |

Aa2 |

|

7,725 |

7,399 |

|

|

California Franchise Tax Board Ctfs. of Prtn. Rfdg. 5.5% 10/1/06 |

A1 |

|

1,825 |

1,949 |

|

|

California Gen. Oblig.: |

|

|

|

|

|

|

Rfdg. 4.75% 2/1/19 (FGIC Insured) |

Aaa |

|

2,000 |

1,880 |

|

|

3.6%, tender 6/1/01 (c) |

Aa3 |

|

25,000 |

24,850 |

|

|

4.5% 12/1/14 |

Aa3 |

|

2,250 |

2,151 |

|

|

4.5% 12/1/24 (FGIC Insured) |

Aaa |

|

5,000 |

4,337 |

|

|

5% 10/1/18 |

Aa3 |

|

5,000 |

4,906 |

|

|

5.25% 10/1/14 |

Aa3 |

|

3,000 |

3,076 |

|

|

5.25% 10/1/17 |

Aa3 |

|

1,500 |

1,513 |

|

|

5.5% 6/1/28 |

Aa3 |

|

5,000 |

5,027 |

|

|

5.75% 5/1/30 |

Aa3 |

|

3,080 |

3,167 |

|

|

6.6% 2/1/09 |

Aa3 |

|

3,000 |

3,488 |

|

|

6.75% 8/1/10 |

Aa3 |

|

5,675 |

6,749 |

|

|

California Health Facilities Fing. Auth. Rev.: |

|

|

|

|

|

|

(Cedars-Sinai Med. Ctr. Proj.) Series A: |

|

|

|

|

|

|

6.125% 12/1/30 |

A2 |

|

6,700 |

6,787 |

|

|

6.25% 12/1/34 |

A2 |

|

15,000 |

15,302 |

|

|

(Kaiser Permante Proj.) Series A, 5.55% 8/15/25 (MBIA Insured) |

Aaa |

|

4,720 |

4,733 |

|

|

Rfdg.: |

|

|

|

|

|

|

(Catholic Health Care West Proj.): |

|

|

|

|

|

|

Series 1988 A, 5% 7/1/06 |

Baa1 |

|

3,135 |

3,021 |

|

|

Series A: |

|

|

|

|

|

|

4.5% 7/1/02 |

Baa1 |

|

7,065 |

6,943 |

|

|

4.5% 7/1/03 |

Baa1 |

|

1,210 |

1,175 |

|

|

4.5% 7/1/04 |

Baa1 |

|

1,500 |

1,436 |

|

|

5% 7/1/01 |

Baa1 |

|

3,615 |

3,612 |

|

|

(Children's Hosp. Proj.) 6% 7/1/03 |

Aaa |

|

1,200 |

1,258 |

|

|

Municipal Bonds - continued |

|||||

|

Moody's Ratings (unaudited) (a) |

Principal Amount (000s) |

Value (Note 1) (000s) |

|||

|

California - continued |

|||||

|

California Hsg. Fin. Agcy. Home Mtg. Rev. |

Aaa |

|

$ 860 |

$ 856 |

|

|

California Hsg. Fin. Agcy. Rev.: |

|

|

|

|

|

|

(Cap. Appreciation) (Home Mtg. Prog.): |

|

|

|

|

|

|

Series 1983 A, 0% 2/1/15 |

Aa2 |

|

8,187 |

2,527 |

|

|

Series 1983 B, 0% 8/1/15 |

Aa2 |

|

170 |

52 |

|

|

Series C, 0% 8/1/21 (c) |

Aa2 |

|

340 |

69 |

|

|

(Home Mtg. Prog.): |

|

|

|

|

|

|

Series I, 4.95% 8/1/28 (MBIA Insured) (c) |

Aaa |

|

2,615 |

2,610 |

|

|

Series J, 4.85% 8/1/27 (MBIA Insured) (c) |

Aaa |

|

3,380 |

3,346 |

|

|

California Poll. Cont. Fing. Auth. Poll. Cont. Rev.: |

|

|

|

|

|

|

(Gen. Motors Corp. Proj.) 5.5% 4/1/08 |

A3 |

|

1,500 |

1,508 |

|

|

(Pacific Gas & Elec. Co. Proj.) Series B, 6.35% 6/1/09 (MBIA Insured) (c) |

Aaa |

|

7,000 |

7,410 |

|

|

Rfdg. (San Diego Gas & Elec. Co. Proj.) |

A2 |

|

4,000 |

4,353 |

|

|

California Pub. Cap. Impt. Fin. Auth. Rev. (A Joint Powers Agcy. Proj.) Series B, 8.1% 3/1/18 (MBIA Insured) |

Aaa |

|

8,560 |

8,636 |

|

|

California Pub. Works Board Lease Rev.: |

|

|

|

|

|

|

(Dept. of Corrections, Madera State |

|

|

|

|

|

|

5.5% 6/1/15 |

A1 |

|

8,250 |

8,745 |

|

|

5.5% 6/1/19 |

A1 |

|

3,000 |

3,025 |

|

|

6% 6/1/07 |

A1 |

|

1,590 |

1,743 |

|

|

(Dept. of Corrections, Susanville State Prison Proj.) Series D, 5.25% 6/1/15 (FSA Insured) |

Aaa |

|

4,000 |

4,179 |

|

|

(Substance Abuse Treatment Facilities |

Aaa |

|

3,000 |

3,124 |

|

|

(Various California State Univ. Projs.): |

|

|

|

|

|

|

Series A: |

|

|

|

|

|

|

6.1% 10/1/06 |

A1 |

|

1,210 |

1,313 |

|

|

6.5% 9/1/04 |

A |

|

1,090 |

1,182 |

|

|

Series B: |

|

|

|

|

|

|

5.5% 6/1/14 |

Aa3 |

|

2,750 |

2,839 |

|

|

5.5% 6/1/19 |

Aa3 |

|

2,000 |

2,018 |

|

|

6.4% 12/1/09 |

Aa3 |

|

3,700 |

4,264 |

|

|

Series C, 5.125% 9/1/22 (AMBAC Insured) |

Aaa |

|

10,000 |

9,699 |

|

|

Rfdg.: |

|

|

|

|

|

|

(California Cmnty. College Projs.) Series A, 5.25% 12/1/16 |

A1 |

|

4,450 |

4,497 |

|

|

Municipal Bonds - continued |

|||||

|

Moody's Ratings (unaudited) (a) |

Principal Amount (000s) |

Value (Note 1) (000s) |

|||

|

California - continued |

|||||

|

California Pub. Works Board Lease Rev.: - continued |

|

|

|

|

|

|

Rfdg.: |

|

|

|

|

|

|

(Dept. of Corrections, Monterey County State Prison Proj.) Series D: |

|

|

|

|

|

|

5.375% 11/1/12 |

A1 |

|

$ 1,250 |

$ 1,308 |

|

|

5.375% 11/1/13 |

A1 |

|

5,055 |

5,246 |

|

|

5.375% 11/1/14 |

A1 |

|

5,000 |

5,151 |

|

|

(Library & Courts Annex Proj.) Series A, 5.5% 5/1/09 |

A1 |

|

1,290 |

1,391 |

|

|

California Statewide Cmnty. Dev. Auth. Rev.: |

|

|

|

|

|

|

(Los Angeles Orthopaedic Hosp. Foundation Proj.) 5.75% 6/1/30 (AMBAC Insured) |

Aaa |

|

10,000 |

10,161 |

|

|

(Sisters Charity Leavenworth Proj.) 5% 12/1/14 |

Aa3 |

|

1,315 |

1,269 |

|

|

Rfdg.: |

|

|

|

|

|

|

(Children's Hosp. Proj.) 6% 6/1/13 |

Aaa |

|

2,470 |

2,762 |

|

|

(Saint Joseph Health Sys. Proj.): |

|

|

|

|

|

|

5.5% 7/1/14 |

Aa3 |

|

9,500 |

9,547 |

|

|

5.5% 7/1/23 |

Aa3 |

|

3,000 |

2,912 |

|

|

(Triad Health Care Hosp. Proj.) 6.25% 8/1/06 (Escrowed to Maturity) (d) |

AA- |

|

5,000 |

5,373 |

|

|

5.616% 7/1/13 (MBIA Insured) |

Aaa |

|

10,000 |

10,214 |

|

|

California Statewide Cmnty. Dev. Auth. Rev. Ctfs. of Prtn.: |

|

|

|

|

|

|

(Catholic Health Care West Proj.) 6% 7/1/09 |

Baa1 |

|

4,785 |

4,841 |

|

|

Rfdg. (Saint Joseph Health Sys. Proj.): |

|

|

|

|

|

|

5.25% 7/1/08 |

Aa3 |

|

2,710 |

2,743 |

|

|

5.5% 7/1/07 |

Aa3 |

|

1,425 |

1,465 |

|

|

California Univ. Rev. (Hsg. Sys. Proj.) Series 1999 AY, 5.875% 11/1/30 (FGIC Insured) |

Aaa |

|

3,000 |

3,122 |

|

|

Campbell Gen. Oblig. Ctfs. of Prtn. Rfdg. (Civic Ctr. Proj.) 6% 10/1/18 |

A2 |

|

4,965 |

5,084 |

|

|

Carson Redev. Agcy. Rfdg.: |

|

|

|

|

|

|

(Area #1 Redev. Proj.): |

|

|

|

|

|

|

6.375% 10/1/12 |

Baa1 |

|

3,965 |

4,146 |

|

|

6.375% 10/1/16 |

Baa1 |

|

2,000 |

2,072 |

|

|

(Area #2 Redev. Proj.) 5.5% 10/1/02 |

Baa2 |

|

100 |

102 |

|

|

Castaic Lake Wtr. Agcy. Ctfs. of Prtn. Rfdg. (Wtr. Sys. Impt. Proj.) Series A: |

|

|

|

|

|

|

7% 8/1/11 (MBIA Insured) |

Aaa |

|

1,500 |

1,821 |

|

|

7% 8/1/13 (MBIA Insured) |

Aaa |

|

4,740 |

5,811 |

|

|

7.25% 8/1/07 (MBIA Insured) |

Aaa |

|

1,755 |

2,065 |

|

|

Municipal Bonds - continued |

|||||

|

Moody's Ratings (unaudited) (a) |

Principal Amount (000s) |

Value (Note 1) (000s) |

|||

|

California - continued |

|||||

|

Central Valley Fing. Auth. Cogeneration Proj. Rev. (Carson Ice Gen. Proj.): |

|

|

|

|

|

|

5.5% 7/1/01 |

BBB- |

|

$ 1,400 |

$ 1,412 |

|

|

6% 7/1/09 |

BBB- |

|

4,800 |

4,993 |

|

|

Coalinga Gen. Oblig. Ctfs. of Prtn. 7% 4/1/10 |

A- |

|

3,505 |

3,580 |

|

|

Contra Costa County Ctfs. of Prtn. (Cap. Appreciation) (Merrithew Mem. Hosp. Proj.): |

|

|

|

|

|

|

0% 11/1/13 (Escrowed to Maturity) (d) |

Aaa |

|

6,805 |

3,500 |

|

|

0% 11/1/14 (Escrowed to Maturity) (d) |

Aaa |

|

3,000 |

1,441 |

|

|

Contra Costa Wtr. District Wtr. Rev. Series G, 5.75% 10/1/14 (MBIA Insured) |

Aaa |

|

2,000 |

2,107 |

|

|

Desert Hosp. District Hosp. Rev. Ctfs. of Prtn. 6.392% 7/28/20 (FSA Insured) (Pre-Refunded to 7/23/02 @ 102) (d) |

Aaa |

|

13,000 |

13,716 |

|

|

Duarte Ctfs. of Prtn. Rfdg. Series A: |

|

|

|

|

|

|

4.625% 4/1/07 |

Baa2 |

|

890 |

843 |

|

|

5% 4/1/11 |

Baa2 |

|

2,000 |

1,866 |

|

|

5% 4/1/12 |

Baa2 |

|

4,210 |

3,869 |

|

|

5% 4/1/13 |

Baa2 |

|

1,830 |

1,658 |

|

|

5.25% 4/1/08 |

Baa2 |

|

2,650 |

2,619 |

|

|

5.25% 4/1/09 |

Baa2 |

|

1,600 |

1,572 |

|

|

Elk Grove Unified School District Spl. Tax Rfdg. (Commty. Facilities District #1 Proj.) 6.5% 12/1/24 (AMBAC Insured) |

Aaa |

|

4,000 |

4,670 |

|

|

Encinitas Union School District (Cap. Appreciation): |

|

|

|

|

|

|

0% 8/1/03 (MBIA Insured) |

Aaa |

|

1,750 |

1,548 |

|

|

0% 8/1/04 (MBIA Insured) |

Aaa |

|

1,750 |

1,483 |

|

|

0% 8/1/10 (MBIA Insured) |

Aaa |

|

1,000 |

634 |

|

|

Escondido Union High School District (Cap. Appreciation): |

|

|

|

|

|

|

0% 11/1/15 (MBIA Insured) (Escrowed to Maturity) (d) |

Aaa |

|

3,000 |

1,358 |

|

|

0% 11/1/16 (MBIA Insured) (Escrowed to Maturity) (d) |

Aaa |

|

3,500 |

1,478 |

|

|

Eureka Unified School District Ctfs. of Prtn. |

Aaa |

|

660 |

687 |

|

|

Fairfield-Suisun Swr. District Swr. Rev. Rfdg. (Cap. Appreciation) Series A: |

|

|

|

|

|

|

0% 5/1/07 (MBIA Insured) |

Aaa |

|

1,635 |

1,220 |

|

|

0% 5/1/08 (MBIA Insured) |

Aaa |

|

2,085 |

1,484 |

|

|

0% 5/1/09 (MBIA Insured) |

Aaa |

|

2,080 |

1,409 |

|

|

Municipal Bonds - continued |

|||||

|

Moody's Ratings (unaudited) (a) |

Principal Amount (000s) |

Value (Note 1) (000s) |

|||

|

California - continued |

|||||

|

Foothill-De Anza Cmnty. College District: |

|

|

|

|

|

|

(Cap. Appreciation) 0% 8/1/15 (MBIA Insured) |

Aaa |

|

$ 2,415 |

$ 1,121 |

|

|

6% 8/1/30 |

Aa2 |

|

10,000 |

10,418 |

|

|

Foothill/Eastern Trans. Corridor Agcy. Toll Road Rev. (Cap. Appreciation) Sr. Lien Series A: |

|

|

|

|

|

|

0% 1/1/04 (Escrowed to Maturity) (d) |

Aaa |

|

1,600 |

1,378 |

|

|

0% 1/1/05 (Escrowed to Maturity) (d) |

Aaa |

|

1,000 |

822 |

|

|

0% 1/1/08 (Escrowed to Maturity) (b)(d) |

Aaa |

|

2,000 |

1,743 |

|

|

0% 1/1/15 (Escrowed to Maturity) (d) |

Aaa |

|

5,000 |

2,364 |

|

|

Foster City Pub. Fing. Auth. Rev. (Foster City Cmnty. Dev. Ln. Prog.) Series A: |

|

|

|

|

|

|

5.5% 9/1/09 |

A- |

|

370 |

389 |

|

|

5.8% 9/1/16 |

A- |

|

1,000 |

1,034 |

|

|

6% 9/1/06 |

A- |

|

1,355 |

1,417 |

|

|

6% 9/1/07 |

A- |

|

1,440 |

1,502 |

|

|

6% 9/1/13 |

A- |

|

1,925 |

1,992 |

|

|

Fremont Unifed School District Alameda County (Cap. Appreciation) Series F, 0% 8/1/09 (MBIA Insured) |

Aaa |

|

1,000 |

670 |

|

|

Fullerton Univ. Foundation Auxillary Organization Rev. Series A: |

|

|

|

|

|

|

5.75% 7/1/25 (MBIA Insured) |

Aaa |

|

1,250 |

1,294 |

|

|

5.75% 7/1/30 (MBIA Insured) |

Aaa |

|

1,000 |

1,032 |

|

|

Glendale Elec. Rev. 6% 2/1/30 (MBIA Insured) |

Aaa |

|

12,245 |

12,838 |

|

|

La Quinta Redev. Agcy. Tax. Allocation Rfdg. (Area #1 Redev. Proj.): |

|

|

|

|

|

|

7.3% 9/1/06 (MBIA Insured) |

Aaa |

|

620 |

720 |

|

|

7.3% 9/1/11 (MBIA Insured) |

Aaa |

|

555 |

689 |

|

|

Local Govt. Fin. Auth. Rev. (Cap. Appreciation) (Oakland Central District Proj.): |

|

|

|

|

|

|

0% 9/1/08 (MBIA Insured) |

Aaa |

|

3,710 |

2,602 |

|

|

0% 9/1/09 (MBIA Insured) |

Aaa |

|

3,565 |

2,379 |

|

|

Long Beach Hbr. Rev.: |

|

|

|

|

|

|

Rfdg. Series A: |

|

|

|

|

|

|

5% 5/15/03 (FGIC Insured) (c) |

Aaa |

|

1,900 |

1,936 |

|

|

5.5% 5/15/08 (FGIC Insured) (c) |

Aaa |

|

8,780 |

9,369 |

|

|

6% 5/15/09 (FGIC Insured) (c) |

Aaa |

|

3,000 |

3,317 |

|

|

6% 5/15/10 (FGIC Insured) (c) |

Aaa |

|

1,000 |

1,107 |

|

|

5.125% 5/15/13 (c) |

Aa3 |

|

12,450 |

12,584 |

|

|

5.5% 5/15/11 (MBIA Insured) (c) |

Aaa |

|

700 |

733 |

|

|

5.5% 5/15/15 (MBIA Insured) (c) |

Aaa |

|

3,710 |

3,790 |

|

|

Municipal Bonds - continued |

|||||

|

Moody's Ratings (unaudited) (a) |

Principal Amount (000s) |

Value (Note 1) (000s) |

|||

|

California - continued |

|||||

|

Long Beach Hbr. Rev.: - continued |

|

|

|

|

|

|

5.75% 5/15/07 (MBIA Insured) (c) |

Aaa |

|

$ 4,845 |

$ 5,194 |

|

|

6% 5/15/06 (MBIA Insured) (c) |

Aaa |

|

3,525 |

3,813 |

|

|

Los Angeles County Ctfs. of Prtn. (Cap. Appreciation): |

|

|

|

|

|

|

(Correctional Facilities Proj.): |

|

|

|

|

|

|

0% 9/1/10 (MBIA Insured) (Escrowed to Maturity) (d) |

Aaa |

|

3,770 |

2,329 |

|

|

0% 9/1/11 (MBIA Insured) (Escrowed to Maturity) (d) |

Aaa |

|

6,400 |

3,724 |

|

|

0% 9/1/13 (MBIA Insured) (Escrowed to Maturity) (d) |

Aaa |

|

3,380 |

1,753 |

|

|

(Disney Parking Proj.): |

|

|

|

|

|

|

0% 3/1/10 |

A3 |

|

2,000 |

1,240 |

|

|

0% 3/1/11 |

A3 |

|

1,950 |

1,135 |

|

|

0% 3/1/12 |

A3 |

|

2,180 |

1,191 |

|

|

0% 3/1/13 |

A3 |

|

6,490 |

3,312 |

|

|

0% 3/1/18 |

A3 |

|

3,000 |

1,071 |

|

|

0% 3/1/19 |

A3 |

|

3,175 |

1,059 |

|

|

0% 3/1/20 |

A3 |

|

1,000 |

312 |

|

|

Los Angeles County Metro. Trans. Auth. Sales Tax Rev. Rfdg. (Proposition A Proj.) First Tier Sr. Series C, 4.75% 7/1/17 (AMBAC Insured) |

Aaa |

|

3,310 |

3,154 |

|

|

Los Angeles County Pub. Works Fing. Auth. Rev.

(Reg'l. Park & Open Space District Proj.) |

Aa3 |

|

6,000 |

5,834 |

|

|

Los Angeles Dept. Arpts. Rev. (Los Angeles Int'l.

Arpt. Proj.) Series D, 5.625% 5/15/12 |

Aaa |

|

1,000 |

1,043 |

|

|

Los Angeles Dept. Wtr. & Pwr. Elec. Plant Rev.: |

|

|

|

|

|

|

Rfdg.: |

|

|

|

|

|

|

Second Issue: |

|

|

|

|

|

|

4.75% 11/15/19 (MBIA Insured) |

Aaa |

|

4,000 |

3,723 |

|

|

5.25% 11/15/26 (MBIA Insured) |

Aaa |

|

16,690 |

16,342 |

|

|

5.4% 11/15/31 (MBIA Insured) |

Aaa |

|

1,875 |

1,853 |

|

|

4.75% 8/15/12 (FGIC Insured) |

Aaa |

|

6,035 |

6,077 |

|

|

4.75% 8/15/16 (FGIC Insured) |

Aaa |

|

2,700 |

2,620 |

|

|

6.375% 2/1/20 |

Aa3 |

|

1,000 |

1,038 |

|

|

Second Issue: |

|

|

|

|

|

|

4.75% 10/15/20 |

Aa3 |

|

1,800 |

1,645 |

|

|

6.75% 10/15/04 (AMBAC Insured) |

Aaa |

|

2,400 |

2,631 |

|

|

9% 10/15/01 |

Aa3 |

|

110 |

116 |

|

|

Municipal Bonds - continued |

|||||

|

Moody's Ratings (unaudited) (a) |

Principal Amount (000s) |

Value (Note 1) (000s) |

|||

|

California - continued |

|||||

|

Los Angeles Dept. Wtr. & Pwr. Wtrwks. Rev.: |

|

|

|

|

|

|

Rfdg.: |

|

|

|

|

|

|

5.5% 10/15/10 |

Aa3 |

|

$ 2,630 |

$ 2,842 |

|

|

5.5% 10/15/11 (MBIA Insured) |

Aaa |

|

3,670 |

3,948 |

|

|

6.1% 10/15/39 (FGIC Insured) |

Aaa |

|

6,000 |

6,319 |

|

|

6.4% 5/15/28 |

Aa |

|

5,000 |

5,153 |

|

|

Los Angeles Gen. Oblig. Ctfs. of Prtn. (Dept. Pub. Social Svcs. Proj.) Series A, 5.5% 8/1/24 (AMBAC Insured) |

Aaa |

|

3,700 |

3,734 |

|

|

Los Angeles Hbr. Dept. Rev.: |

|

|

|

|

|

|

Series B: |

|

|

|

|

|

|

5% 8/1/03 (c) |

Aa3 |

|

2,500 |

2,555 |

|

|

5.25% 11/1/03 (c) |

Aa3 |

|

1,250 |

1,289 |

|

|

5.25% 11/1/06 (c) |

Aa3 |

|

7,380 |

7,750 |

|

|

5.25% 11/1/07 (c) |

Aa3 |

|

4,290 |

4,522 |

|

|

5.25% 11/1/10 (c) |

Aa3 |

|

9,105 |

9,501 |

|

|

5.25% 11/1/11 (c) |

Aa3 |

|

7,095 |

7,365 |

|

|

5.3% 8/1/06 (c) |

Aa3 |

|

2,000 |

2,102 |

|

|

5.5% 8/1/08 (c) |

Aa3 |

|

1,505 |

1,601 |

|

|

7.6% 10/1/18 (Escrowed to Maturity) (d) |

AAA |

|

14,810 |

18,841 |

|

|

Los Angeles Unified School District Series A, 6% 7/1/14 (FGIC Insured) |

Aaa |

|

1,200 |

1,354 |

|

|

M-S-R Pub. Pwr. Agcy. San Juan Proj. Rev. Rfdg. Series D, 6.75% 7/1/20 (MBIA Insured) (Escrowed to Maturity) (d) |

Aaa |

|

2,500 |

2,868 |

|

|

Manhattan Beach Unified School District |

Aaa |

|

975 |

651 |

|

|

Metro. Wtr. District Southern California Wtrwks. Rev.: |

|

|

|

|

|

|

Rfdg. Series A, 4.75% 7/1/22 |

Aa2 |

|

10,000 |

9,052 |

|

|

Series A: |

|

|

|

|

|

|

5% 7/1/26 |

Aa2 |

|

5,050 |

4,724 |

|

|

5% 7/1/30 (MBIA Insured) |

Aaa |

|

3,500 |

3,279 |

|

|

5.95% 8/5/22 (Pre-Refunded to |

Aa2 |

|

2,600 |

2,734 |

|

|

Modesto Gen. Oblig. Ctfs. of Prtn.: |

|

|

|

|

|

|

(Cmnty. Ctr. Refing. Proj.) Series A, 5% 11/1/23 (AMBAC Insured) |

Aaa |

|

2,500 |

2,401 |

|

|

(Golf Course Refing. Proj.) Series B, 5% 11/1/23 (FGIC Insured) |

Aaa |

|

1,585 |

1,522 |

|

|

Municipal Bonds - continued |

|||||

|

Moody's Ratings (unaudited) (a) |

Principal Amount (000s) |

Value (Note 1) (000s) |

|||

|

California - continued |

|||||

|

Modesto Irrigation District: |

|

|

|

|

|

|

Ctfs. of Prtn. (Geysers Geothermal Pwr. Proj.) Series 1986 A, 5% 10/1/17 (Escrowed to Maturity) (d) |

A1 |

|

$ 5,000 |

$ 4,909 |

|

|

Ctfs. of Prtn. Rfdg. & Cap. Impts. (Cap. Appreciation) Series A: |

|

|

|

|

|

|

0% 10/1/08 (MBIA Insured) (Escrowed to Maturity) (d) |

Aaa |

|

2,270 |

1,571 |

|

|

0% 10/1/09 (MBIA Insured) (Escrowed to Maturity) (d) |

Aaa |

|

2,270 |

1,495 |

|

|

0% 10/1/10 (MBIA Insured) (Escrowed to Maturity) (d) |

Aaa |

|

2,270 |

1,409 |

|

|

Moreno Valley Unified School District Ctfs. of Prtn. (Land Acquisition Proj.) Series F, 6.7% 9/1/11 (FSA Insured) (Pre-Refunded to 9/1/02 @ 102) (d) |

Aaa |

|

2,230 |

2,334 |

|

|

Northern California Pwr. Agcy. Multiple Cap. Facilities Rev. 6.538% 8/1/25 (MBIA Insured) (Pre-Refunded to 9/3/02 @ 102) (d) |

Aaa |

|

7,600 |

8,043 |

|

|

Northern California Pwr. Agcy. Pub. Pwr. Rev. Rfdg. (Hydro Elec. #1 Proj.) Series A, 7.5% 7/1/23 (AMBAC Insured) (Pre-Refunded to 7/1/21 @ 100) (d) |

Aaa |

|

3,825 |

4,800 |

|

|

Northern California Transmission Auth. Rev. |

Aaa |

|

7,100 |

8,681 |

|

|

Oakland Gen. Oblig. Ctfs. of Prtn. Rfdg. |

Aaa |

|

2,750 |

2,060 |

|

|

Oakland Redev. Agcy. Sub Tax Allocation (Central District Redev. Proj.) 5% 9/1/21 (MBIA Insured) |

Aaa |

|

1,000 |

959 |

|

|

Ontario Redev. Fing. Auth. Rev. (Cap. Appreciation) (Ctr. City Cimarron #1 Proj.): |

|

|

|

|

|

|

0% 8/1/08 (MBIA Insured) |

Aaa |

|

3,255 |

2,291 |

|

|

0% 8/1/09 (MBIA Insured) |

Aaa |

|

3,260 |

2,184 |

|

|

0% 8/1/10 (MBIA Insured) |

Aaa |

|

3,255 |

2,065 |

|

|

Orange County Arpt. Rev. Rfdg.: |

|

|

|

|

|

|

5.5% 7/1/02 (MBIA Insured) (c) |

Aaa |

|

2,000 |

2,046 |

|

|

5.5% 7/1/04 (MBIA Insured) (c) |

Aaa |

|

2,000 |

2,086 |

|

|

5.5% 7/1/11 (MBIA Insured) (c) |

Aaa |

|

4,000 |

4,224 |

|

|

6% 7/1/05 (MBIA Insured) (c) |

Aaa |

|

3,000 |

3,217 |

|

|

6% 7/1/07 (MBIA Insured) (c) |

Aaa |

|

9,135 |

9,982 |

|

|

Municipal Bonds - continued |

|||||

|

Moody's Ratings (unaudited) (a) |

Principal Amount (000s) |

Value (Note 1) (000s) |

|||

|

California - continued |

|||||

|

Orange County Pub. Fin. Auth. Waste Mgt. Sys. Rev. Rfdg.: |

|

|

|

|

|

|

5.75% 12/1/09 (AMBAC Insured) (c) |

Aaa |

|

$ 3,620 |

$ 3,954 |

|

|

5.75% 12/1/11 (AMBAC Insured) (c) |

Aaa |

|

4,000 |

4,369 |

|

|

Orange County Wtr. District Ctfs. of Prtn. Rfdg. Series A, 5.5% 8/15/09 (AMBAC Insured) |

Aaa |

|

1,000 |

1,051 |

|

|

Palmdale Elementary School District Spl. Tax Rfdg. (Cmnty. Facilities District #90-1) 5.8% 8/1/29 (FSA Insured) |

Aaa |

|

6,410 |

6,627 |

|

|

Placer County Wtr. Agcy. Rev. (Middle Fork Proj.) Series A, 3.75% 7/1/12 |

A+ |

|

8,830 |

8,035 |

|

|

Placer County Wtr. Agcy. Wtr. Rev. Ctfs. of Prtn. (Cap. Impt. Projs.) 5.5% 7/1/29 (AMBAC Insured) |

Aaa |

|

3,000 |

3,015 |

|

|

Pleasanton Joint Powers Fing. Auth. Rev. (Reassessment Proj.) Series A: |

|

|

|

|

|

|

5.7% 9/2/01 |

Baa1 |

|

1,145 |

1,160 |

|

|

5.8% 9/2/02 |

Baa1 |

|

4,970 |

5,103 |

|

|

6% 9/2/05 |

Baa1 |

|

2,135 |

2,259 |

|

|

6.15% 9/2/12 |

Baa1 |

|

12,205 |

12,822 |

|

|

Pomona Unified School District Series C, 6% 8/1/30 (FGIC Insured) |

Aaa |

|

4,535 |

4,746 |

|

|

Port of Oakland Port Rev.: |

|

|

|

|

|

|

Rfdg. (Cap. Appreciation) Series F: |

|

|

|

|

|

|

0% 11/1/05 (MBIA Insured) |

Aaa |

|

300 |

240 |

|

|

0% 11/1/06 (MBIA Insured) |

Aaa |

|

2,890 |

2,211 |

|

|

0% 11/1/07 (MBIA Insured) |

Aaa |

|

4,250 |

3,103 |

|

|

Series G: |

|

|

|

|

|

|

5.375% 11/1/08 (MBIA Insured) (c) |

Aaa |

|

1,805 |

1,917 |

|

|

6% 11/1/07 (MBIA Insured) (c) |

Aaa |

|

1,650 |

1,809 |

|

|

Rancho Wtr. District Fing. Auth. Rev. 6.427% 8/17/21 (AMBAC Insured) (Pre-Refunded to 9/11/01 @ 102) (d) |

Aaa |

|

6,900 |

7,195 |

|

|

Redding Elec. Sys. Rev. Ctfs. of Prtn. Rfdg. (Cap. Appreciation) Series A: |

|

|

|

|

|

|

0% 6/1/06 (FGIC Insured) |

Aaa |

|

1,730 |

1,348 |

|

|

0% 6/1/07 (FGIC Insured) |

Aaa |

|

1,890 |

1,406 |

|

|

0% 6/1/08 (FGIC Insured) |

Aaa |

|

1,300 |

922 |

|

|

Richmond Redev. Agcy. Tax Allocation Rev. |

Aaa |

|

105 |

112 |

|

|

Municipal Bonds - continued |

|||||

|

Moody's Ratings (unaudited) (a) |

Principal Amount (000s) |

Value (Note 1) (000s) |

|||

|

California - continued |

|||||

|

Riverside County Asset Leasing Corp. Leasehold Rev. (Riverside County Hosp. Proj.): |

|

|

|

|

|

|

Series A: |

|

|

|

|

|

|

5.75% 6/1/01 (MBIA Insured) |

Aaa |

|

$ 1,250 |

$ 1,266 |

|

|

6.375% 6/1/09 (MBIA Insured) |

Aaa |

|

5,000 |

5,369 |

|

|

6.5% 6/1/12 (MBIA Insured) |

Aaa |

|

15,500 |

18,158 |

|

|

Series B, 5.7% 6/1/16 (MBIA Insured) |

Aaa |

|

1,950 |

2,069 |

|

|

Riverside County Pub.Fing. Auth. Tax Allocation Rev. (Redev. Projs.) Series A: |

|

|

|

|

|

|

4.8% 10/1/07 |

Baa2 |

|

1,080 |

1,092 |

|

|

5% 10/1/08 |

Baa2 |

|

1,135 |

1,162 |

|

|

5% 10/1/09 |

Baa2 |

|

1,140 |

1,163 |

|

|

5.1% 10/1/10 |

Baa2 |

|

1,245 |

1,267 |

|

|

5.25% 10/1/12 |

Baa2 |

|

1,375 |

1,395 |

|

|

5.5% 10/1/22 |

Baa2 |

|

4,500 |

4,263 |

|

|

Riverside County Redev. Agcy. Tax Allocation |

|

|

|

|

|

|

7.5% 10/1/10 (Pre-Refunded to |

- |

|

1,000 |

1,055 |

|

|

7.5% 10/1/26 (Pre-Refunded to |

- |

|

2,500 |

2,639 |

|

|

Riverside Unified School District Ctfs. of Prtn.

(Cap. Appreciation) (Land Acquisition Proj.)

Series B, 7.375% 9/1/26 (FSA Insured) |

Aaa |

|

5,420 |

5,705 |

|

|

Sacramento City Fing. Auth. Lease Rev. Rfdg. Series A, 5.4% 11/1/20 (AMBAC Insured) |

Aaa |

|

2,000 |

2,034 |

|

|

Sacramento City Unified School District Series A, 6% 7/1/29 (FGIC Insured) |

Aaa |

|

6,300 |

6,614 |

|

|

Sacramento Cogeneration Auth. Cogeneration Proj. Rev. (Procter & Gamble Proj.): |

|

|

|

|

|

|

5.9% 7/1/02 |

BBB- |

|

1,000 |

1,024 |

|

|

6% 7/1/03 |

BBB- |

|

700 |

727 |

|

|

6.375% 7/1/10 |

BBB- |

|

700 |

749 |

|

|

6.5% 7/1/21 (Pre-Refunded to |

AAA |

|

3,200 |

3,588 |

|

|

Sacramento Muni. Util. District Elec. Rev.: |

|

|

|

|

|

|

Rfdg.: |

|

|

|

|

|

|

Series L, 5.125% 7/1/22 (MBIA Insured) |

Aaa |

|

4,000 |

3,880 |

|

|

Series M, 5.25% 7/1/28 |

A2 |

|

6,500 |

6,208 |

|

|

5.45% 11/15/08 (FGIC Insured) |

Aaa |

|

17,700 |

18,647 |

|

|

Sacramento Pwr. Auth. Cogeneration Proj. Rev.: |

|

|

|

|

|

|

6% 7/1/22 |

BBB- |

|

2,700 |

2,727 |

|

|

Municipal Bonds - continued |

|||||

|

Moody's Ratings (unaudited) (a) |

Principal Amount (000s) |

Value (Note 1) (000s) |

|||

|

California - continued |

|||||

|

Sacramento Pwr. Auth. Cogeneration Proj. Rev.: - continued |

|

|

|

|

|

|

6.5% 7/1/06 |

BBB- |

|

$ 4,500 |

$ 4,902 |

|

|

6.5% 7/1/07 |

BBB- |

|

2,000 |

2,200 |

|

|

6.5% 7/1/08 |

BBB- |

|

1,000 |

1,102 |

|

|

San Bernardino County: |

|

|

|

|

|

|

Ctfs. of Prtn (Cap. Facilities Proj.) Series B, 6.875% 8/1/24 (Escrowed to Maturity) (d) |

AAA |

|

8,500 |

10,252 |

|

|

Ctfs. of Prtn. Rfdg. (Med. Ctr. Fing. Prog.) |

A3 |

|

10,000 |

9,486 |

|

|

San Diego County Ctfs. of Prtn (Burnham |

|

|

|

|

|

|

5.7% 9/1/11 |

Baa3 |

|

800 |

847 |

|

|

6.25% 9/1/29 |

Baa3 |

|

6,800 |

6,932 |

|

|

San Diego County Wtr. Auth. Wtr. Rev. Ctfs. of Prtn. 5.632% 4/25/07 (FGIC Insured) |

Aaa |

|

5,000 |

5,338 |

|

|

San Diego Multi-Family Hsg. Rev. (Island Gardens Apts. Proj.) Series B, 9.5% 10/20/20 |

AAA |

|

1,585 |

1,585 |

|

|

San Diego Wtr. Util. Fund Ctfs. of Prtn. 4.75% 8/1/28 (FGIC Insured) |

Aaa |

|

10,000 |

8,910 |

|

|

San Francisco Bay Area Rapid Trans. District Sales Tax Rev. Rfdg. 5.25% 7/1/18 |

Aa3 |

|

4,500 |

4,528 |

|

|

San Francisco Bay Area Trans. Fing. Auth. (Bridge Toll Proj.): |

|

|

|

|

|

|

4.75% 8/1/01 (American Cap. Access |

A |

|

1,000 |

1,007 |

|

|

5% 8/1/02 (American Cap. Access |

A |

|

1,000 |

1,015 |

|

|

5.5% 8/1/05 (American Cap. Access |

A |

|

1,000 |

1,049 |

|

|

5.75% 2/1/07 (American Cap. Access |

A |

|

1,500 |

1,601 |

|

|

San Francisco City & County Arpt. Commission Int'l. Arpt. Rev.: |

|

|

|

|

|

|

(SFO Fuel Co. Proj.) Series A: |

|

|

|

|

|

|

5.125% 1/1/17 (AMBAC Insured) (c) |

Aaa |

|

6,000 |

5,898 |

|

|

5.25% 1/1/18 (AMBAC Insured) (c) |

Aaa |

|

4,515 |

4,463 |

|

|

5.25% 1/1/19 (AMBAC Insured) (c) |

Aaa |

|

4,750 |

4,667 |

|

|

Issue 10 A, Second Series 5.3% 5/1/05 (MBIA Insured) (c) |

Aaa |

|

2,805 |

2,920 |

|

|

Issue 18A, Second Series 6% 5/1/05 |

Aaa |

|

2,375 |

2,542 |

|

|

Municipal Bonds - continued |

|||||

|

Moody's Ratings (unaudited) (a) |

Principal Amount (000s) |

Value (Note 1) (000s) |

|||

|

California - continued |

|||||

|

San Francisco City & County Arpt. Commission Int'l. Arpt. Rev.: - continued |

|

|

|

|

|

|

Issue 22, Second Series 6% 5/1/03 |

Aaa |

|

$ 1,850 |

$ 1,928 |

|

|

Rfdg.: |

|

|

|

|

|

|

Second Series Issue 20, 4.5% 5/1/13 |

Aaa |

|

3,030 |

2,938 |

|

|

Second Series Issue 3, 6.1% 5/1/13 |

Aaa |

|

2,650 |

2,788 |

|

|

Second Series: |

|

|

|

|

|

|

Issue 09A, 5.125% 5/1/07 |

Aaa |

|

2,000 |

2,070 |

|

|

Issue 10A, 5.3% 5/1/06 (MBIA Insured) (c) |

Aaa |

|

3,680 |

3,851 |

|

|

Issue 12A, 5.625% 5/1/08 |

Aaa |

|

1,625 |

1,731 |

|

|

Issue 15A: |

|

|

|

|

|

|

5.5% 5/1/07 (FSA Insured) (c) |

Aaa |

|

5,680 |

6,033 |

|

|

5.5% 5/1/09 (FSA Insured) (c) |

Aaa |

|

1,355 |

1,449 |

|

|

5.6% 5/1/02 (FSA Insured) (c) |

Aaa |

|

4,295 |

4,388 |

|

|

Issue 16A: |

|

|

|

|

|

|

5.375% 5/1/18 (FSA Insured) (c) |

Aaa |

|

5,035 |

5,041 |

|

|

5.5% 5/1/06 (FSA Insured) (c) |

Aaa |

|

1,850 |

1,954 |

|

|

5.5% 5/1/08 (FSA Insured) (c) |

Aaa |

|

2,945 |

3,142 |

|

|

Issue 18A, 5.25% 5/1/11 (MBIA Insured) (c) |

Aaa |

|

3,280 |

3,413 |

|

|

Issue 23A: |

|

|

|

|

|

|

5.5% 5/1/07 (FGIC Insured) (c) |

Aaa |

|

1,045 |

1,110 |

|

|

5.5% 5/1/08 (FGIC Insured) (c) |

Aaa |

|

2,755 |

2,939 |

|

|

San Francisco City & County Pub. Util.

Commission Wtr. Rev. Rfdg. Series A, |

A1 |

|

1,000 |

1,066 |

|

|

San Francisco City & County Redev. Fing. Auth. Tax Allocation Rev.: |

|

|

|

|

|

|

(Cap. Appreciation) Series A: |

|

|

|

|

|

|

0% 8/1/08 (FGIC Insured) |

Aaa |

|

1,085 |

764 |

|

|

0% 8/1/09 (FGIC Insured) |

Aaa |

|

1,085 |

727 |

|

|

0% 8/1/10 (FGIC Insured) |

Aaa |

|

1,085 |

688 |

|

|

Rfdg. (Cap. Appreciation) (San Francisco

Redev. Proj.) Series B, 0% 8/1/10 |

Aaa |

|

1,475 |

936 |

|

|

San Francisco City & County Swr. Rev. (Cap. Appreciation) Series B: |

|

|

|

|

|

|

0% 10/1/06 (FGIC Insured) |

Aaa |

|

3,690 |

2,834 |

|

|

0% 10/1/07 (FGIC Insured) |

Aaa |

|

4,770 |

3,496 |

|

|

Municipal Bonds - continued |

|||||

|

Moody's Ratings (unaudited) (a) |

Principal Amount (000s) |

Value (Note 1) (000s) |

|||

|

California - continued |

|||||

|

San Francisco City & County Swr. Rev. (Cap. Appreciation) Series B: - continued |

|

|

|

|

|

|

0% 10/1/08 (FGIC Insured) |

Aaa |

|

$ 1,600 |

$ 1,118 |

|

|

San Joaquin County Ctfs. of Prtn. (Gen. Hosp. Proj.) 5.7% 9/1/01 (Escrowed to Maturity) (d) |

A2 |

|

2,250 |

2,287 |

|

|

San Joaquin Hills Trans. Corridor Agcy. Toll Road Rev.: |

|

|

|

|

|

|

(Cap. Appreciation) Jr. Lien: |

|

|

|

|

|

|

0% 1/1/07 (Escrowed to Maturity) (d) |

Aaa |

|

3,000 |

2,267 |

|

|

0% 1/1/08 (Escrowed to Maturity) (d) |

Aaa |

|

4,400 |

3,170 |

|

|

Jr. Lien, 0% 1/1/12 (Escrowed to Maturity) (d) |

Aaa |

|

15,000 |

8,586 |

|

|

Rfdg. Series A, 0% 1/15/10 (MBIA Insured) |

Aaa |

|

2,235 |

1,430 |

|

|

San Jose Arpt. Rev. Rfdg. 5.875% 3/1/07 |

Aaa |

|

1,905 |

2,084 |

|

|

San Jose Redev. Agcy. Tax Allocation (Merged Area Redev. Proj.): |

|

|

|

|

|

|

4.75% 8/1/18 (AMBAC Insured) |

Aaa |

|

1,910 |

1,798 |

|

|

4.75% 8/1/29 (AMBAC Insured) |

Aaa |

|

7,150 |

6,351 |

|

|

Sanger Unified School District Rfdg. 5.6% 8/1/23 (MBIA Insured) |

Aaa |

|

3,000 |

3,135 |

|

|

Santa Barbara High School District Series A: |

|

|

|

|

|

|

5.75% 8/1/25 (FGIC Insured) |

Aaa |

|

4,650 |

4,793 |

|

|

5.75% 8/1/30 (FGIC Insured) |

Aaa |

|

7,490 |

7,697 |

|

|

Santa Clara County Fing. Auth. Lease Rev. (VMC Facilities Replacement Proj.) Series A, 7.75% 11/15/09 (AMBAC Insured) |

Aaa |

|

3,725 |

4,668 |

|

|

Santa Clara County Trans. District Sales Tax Rev. Rfdg. Series A, 5.25% 6/1/21 |

AA |

|

8,500 |

8,362 |

|

|

Santa Cruz City Elementary School District |

Aaa |

|

2,730 |

2,818 |

|

|

Santa Cruz City High School District Series B: |

|

|

|

|

|

|

5.75% 8/1/26 (FGIC Insured) |

Aaa |

|

2,380 |

2,457 |

|

|

6% 8/1/29 (FGIC Insured) |

Aaa |

|

6,770 |

7,110 |

|

|

Santa Margarita/Dana Point Auth. Rev. Rfdg. & Impt. (Dists. 1, 2, 2A & 8 Proj.) Series A: |

|

|

|

|

|

|

7.25% 8/1/07 (MBIA Insured) |

Aaa |

|

2,200 |

2,588 |

|

|

7.25% 8/1/08 (MBIA Insured) |

Aaa |

|

1,780 |

2,133 |

|

|

7.25% 8/1/12 (MBIA Insured) |

Aaa |

|

1,865 |

2,329 |

|

|

Santa Monica Redev. Agcy. Tax Allocation |

Aaa |

|

8,395 |

8,670 |

|

|

Municipal Bonds - continued |

|||||

|

Moody's Ratings (unaudited) (a) |

Principal Amount (000s) |

Value (Note 1) (000s) |

|||

|

California - continued |

|||||

|

South Orange County Pub. Fing. Auth. Spl. Tax Rev.: |

|

|

|

|

|

|

(Foothill Area Proj.) Series C: |

|

|

|

|

|

|

7.5% 8/15/06 (FGIC Insured) |

Aaa |

|

$ 2,000 |

$ 2,341 |

|

|

7.5% 8/15/07 (FGIC Insured) |

Aaa |

|

2,290 |

2,730 |

|

|

8% 8/15/09 (FGIC Insured) |

Aaa |

|

3,650 |

4,620 |

|

|

Rfdg. Sr. Lien Series A, 7% 9/1/10 |

Aaa |

|

2,300 |

2,764 |

|

|

Southern California Pub. Pwr. Auth. Pwr. Proj. Rev.: |

|

|

|

|

|

|

(Multiple Proj.): |

|

|

|

|

|

|

6.75% 7/1/10 |

A |

|

1,400 |

1,627 |

|

|

6.75% 7/1/11 |

A |

|

6,500 |

7,611 |

|

|

(Multiple Projs.): |

|

|

|

|

|

|

6.75% 7/1/01 |

A |

|

1,520 |

1,554 |

|

|

7% 7/1/05 |

A |

|

920 |

946 |

|

|

Rfdg.: |

|

|

|

|

|

|

(Mead Adelanto Proj.) Series A, 4.75% 7/1/16 (AMBAC Insured) |

Aaa |

|

2,000 |

1,941 |

|

|

(Palo Verde Proj.) Series A, 5% 7/1/15 (AMBAC Insured) (Escrowed to Maturity) (d) |

Aaa |

|

1,000 |

984 |

|

|

Stanislaus County Ctfs. of Prtn. Rfdg. (Cap. Impt. Prog.) Series A, 5.25% 5/1/14 (MBIA Insured) |

Aaa |

|

1,500 |

1,541 |

|

|

Sulpher Springs Unified School District Series A: |

|

|

|

|

|

|

0% 9/1/07 (MBIA Insured) |

Aaa |

|

4,445 |

3,270 |

|

|

0% 9/1/08 (MBIA Insured) |

Aaa |

|

4,745 |

3,328 |

|

|

0% 9/1/09 (MBIA Insured) |

Aaa |

|

2,485 |

1,658 |

|

|

0% 9/1/12 (MBIA Insured) |

Aaa |

|

2,750 |

1,543 |

|

|

Tahoe-Truckee Joint Unified School District |

Aaa |

|

6,625 |

4,186 |

|

|

Univ. of California Rev. Rfdg. (Multiple Purp. Projs.) Series C, 9% 9/1/02 (AMBAC Insured) |

Aaa |

|

100 |

109 |

|

|

Upland Ctfs. of Prtn. Rfdg. (San Antonio Cmnty. Hosp. Proj.): |

|

|

|

|

|

|

5.25% 1/1/08 |

A |

|

3,700 |

3,673 |

|

|

5.25% 1/1/13 |

A |

|

8,500 |

8,290 |

|

|

Ventura Unified School District Series D, 5.875% 8/1/30 (FSA Insured) |

AAA |

|

1,645 |

1,706 |

|

|

West Covina Ctfs. of Prtn. (Queen of the Valley Hosp. Proj.): |

|

|

|

|

|

|

6% 8/15/03 (Escrowed to Maturity) (d) |

A2 |

|

925 |

975 |

|

|

Municipal Bonds - continued |

|||||

|

Moody's Ratings (unaudited) (a) |

Principal Amount (000s) |

Value (Note 1) (000s) |

|||

|

California - continued |

|||||

|

West Covina Ctfs. of Prtn. (Queen of the Valley Hosp. Proj.): - continued |

|

|

|

|

|

|

6.125% 8/15/04 (Escrowed to Maturity) (d) |

A2 |

|

$ 980 |

$ 1,052 |

|

|

Whittier Union High School District Series B, 5.875% 8/1/30 (FSA Insured) |

Aaa |

|

2,405 |

2,494 |

|

|

|

1,228,227 |

||||

|

Guam - 0.6% |

|||||

|

Guam Pwr. Auth. Rev. Rfdg. Series A: |

|

|

|

|

|

|

4% 10/1/01 |

Baa3 |

|

1,500 |

1,496 |

|

|

4% 10/1/02 |

Baa3 |

|

2,425 |

2,415 |

|

|

4% 10/1/03 |

Baa3 |

|

1,795 |

1,781 |

|

|

4% 10/1/04 |

Baa3 |

|

1,620 |

1,601 |

|

|

|

7,293 |

||||

|

Puerto Rico - 3.7% |

|||||

|

Puerto Rico Commonwealth Gen. Oblig.: |

|

|

|

|

|

|

(Pub. Impt. Proj.): |

|

|

|

|

|

|

5% 7/1/01 |

Baa1 |

|

4,000 |

4,025 |

|

|

5% 7/1/02 |

Baa1 |

|

4,305 |

4,359 |

|

|

5.25% 7/1/13 (MBIA Insured) |

Aaa |

|

6,000 |

6,337 |

|

|

Rfdg. (Pub. Impt. Proj.) 5.5% 7/1/11 |

Baa1 |

|

5,675 |

6,029 |

|

|

8% 7/1/02 |

Baa1 |

|

2,000 |

2,129 |

|

|

Puerto Rico Elec. Pwr. Auth. Pwr. Rev.: |

|

|

|

|

|

|

Series 2000 HH, 5.25% 7/1/09 (FSA Insured) |

Aaa |

|

4,230 |

4,475 |

|

|

Series FF, 5.25% 7/1/06 (MBIA Insured) |

Aaa |

|

2,875 |

3,020 |

|

|

Puerto Rico Muni. Fin. Agcy.: |

|

|

|

|

|

|

Rfdg. Series B: |

|

|

|

|

|

|

5.5% 7/1/02 (FSA Insured) |

Aaa |

|

5,105 |

5,232 |

|

|

5.5% 8/1/02 |

Baa1 |

|

9,000 |

9,200 |

|

|

Series A: |

|

|

|

|

|

|

5% 8/1/02 |

Baa1 |

|

1,805 |

1,827 |

|

|

5.5% 7/1/02 (FSA Insured) |

Aaa |

|

2,845 |

2,916 |

|

|

|

49,549 |

||||

|

TOTAL MUNICIPAL BONDS (Cost $1,232,239) |

1,285,069 |

||||

|

Municipal Notes - 1.6% |

|||

|

Principal Amount (000s) |

Value (Note 1) (000s) |

||

|

California - 1.6% |

|||

|

Los Angeles County Schools Pooled Fing. Prog. Ctfs. of Prtn. TRAN Series B, 5% 10/2/01 (FSA Insured) |

$ 5,000 |

$ 5,053 |

|

|

San Diego Unified School District TRAN 5.25% 10/4/01 |

10,000 |

10,136 |

|

|

Santa Barbara County Gen. Oblig. TRAN 5.25% 10/2/01 |

6,500 |

6,590 |

|

|

TOTAL MUNICIPAL NOTES (Cost $21,639) |

21,779 |

||

|

TOTAL INVESTMENT PORTFOLIO - 98.2% (Cost $1,253,878) |

1,306,848 |

||

|

NET OTHER ASSETS - 1.8% |

23,596 |

||

|

NET ASSETS - 100% |

$ 1,330,444 |

||

|

Security Type Abbreviations |

|

TRAN - TAX AND REVENUE |

|

Legend |

|

(a) S&P credit ratings are used in the absence of a rating by Moody's Investors Service, Inc. |

|

(b) Debt obligation initially issued in zero coupon form which converts to coupon form at a specified rate and date. The rate shown is the rate at period end. |