|

|

|

|

|

|

|

|

|

|

Previous: MML SERIES INVESTMENT FUND, N-30D, 2000-08-23 |

Next: MML SERIES INVESTMENT FUND, N-30D, 2000-08-23 |

| MML Small Cap Value Equity Fund – Letter to Shareholders

|

| |

| MassMutual Expands Fund Offerings

|

| I’d like to announce some exciting additions to the MML Series Investment Fund. Through our comprehensive due diligence

process, we’ve uncovered significant investor demand for a number of fund types and managers that were not previously addressed by our selections. As a result, we’ve added three new funds, listed as follows, with their managers (sub-advisers) in

parentheses: Large Cap Value (Davis Selected Advisers), OTC 100 (Deutsche Asset Management/Bankers Trust Company), and Emerging Growth (RS Investment Management). These new choices span a broad range of investment styles and market sectors—value vs.

growth, active vs. indexed, and large-cap vs. emerging growth. All of our new managers have produced excellent long-term track records, and have passed through our extensive selection process. We will continue to monitor all of our funds carefully so that

you can be assured of access to top-flight investment management talent.

|

Ÿ

|

achieve long-term growth of capital and income

|

Ÿ

|

invest primarily in a diversified portfolio of equity securities of smaller companies (companies with market capitalization, at

the time of purchase, within the range of capitalizations of companies included in the Lipper, Inc. Small Cap category)

|

Ÿ

|

utilize a value-oriented strategy in making investment decisions

|

Ÿ

|

utilize Fundamental analysis to identify companies which

|

| -are of high investment quality or possess a unique product, market position or operating characteristics

|

| -offer above-average levels of profitability or superior growth potential

|

| -are attractively valued in the marketplace

|

| |

What is your outlook?

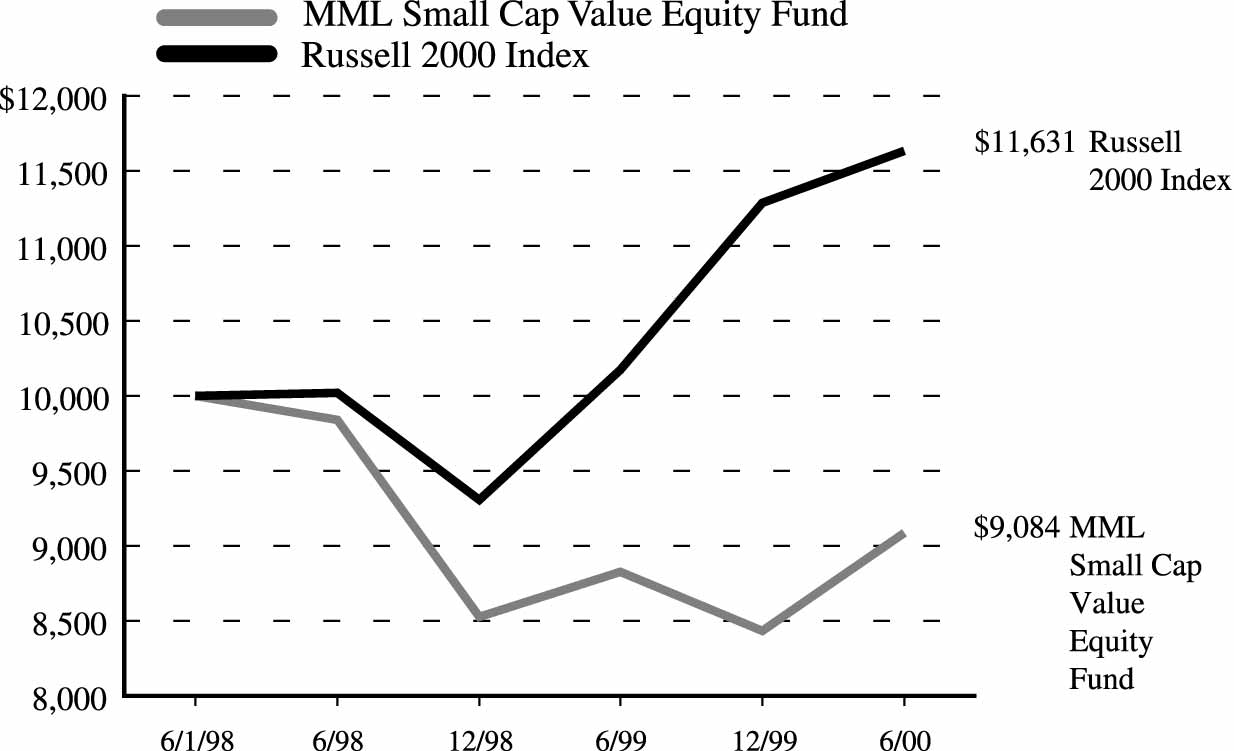

| Year to Date | One Year | Since Inception

Average Annual |

|||||

|---|---|---|---|---|---|---|---|

| 1/1/00 – 6/30/00 | 7/1/99 - 6/30/00 | 6/1/98 - 6/30/00 | |||||

| MML Small Cap

Value Equity Fund |

7.72% | 2.91% | -4.50% | ||||

| Russell 2000 Index | 3.06% | 14.35% | 7.52% | ||||

| ASSETS: | |||

| Investments, at value (cost $25,235,638) (Note 2) | $ 27,057,619 | ||

| Short-term investments, at amortized cost (Note 2) | 3,652,094 | ||

| Total investments | 30,709,713 | ||

| Cash | 5,893,754 | ||

| Receivables from: | |||

| Investments sold | 68,839 | ||

| Interest and dividends | 65,145 | ||

| Investment adviser (Note 3) | 741 | ||

| Total assets | 36,738,192 | ||

| LIABILITIES: | |||

| Payables for: | |||

| Investments purchased | 4,486,404 | ||

| Securities on loan (Note 2) | 1,065,100 | ||

| Affiliates (Note 3): | |||

| Investment management fees | 16,048 | ||

| Accrued expenses and other liabilities | 29,618 | ||

| Total liabilities | 5,597,170 | ||

| NET ASSETS | $ 31,141,022 | ||

| Net assets consist of: | |||

| Paid-in capital | $ 30,601,886 | ||

| Undistributed net investment income | 194,237 | ||

| Accumulated net realized loss on investments | (1,477,082 | ) | |

| Net unrealized appreciation on investments | 1,821,981 | ||

| $ 31,141,022 | |||

| Shares outstanding: | 3,466,885 | ||

| Net asset value, offering price and redemption price per share: | $ 8.98 | ||

| Investment income: (Note 2) | |||

| Dividends | $ 121,472 | ||

| Interest (including securities lending income of $8) | 165,496 | ||

| Total investment income | 286,968 | ||

| Expenses: (Note 3) | |||

| Investment management fees (Note 3) | 80,447 | ||

| Audit and legal fees | 10,634 | ||

| Directors’ fees (Note 3) | 8,496 | ||

| Custody fees | 5,875 | ||

| Other expenses | 2,912 | ||

| Total expenses | 108,364 | ||

| Expenses reimbursed (Note 3) | (14,321 | ) | |

| Net expenses | 94,043 | ||

| Net investment income | 192,925 | ||

| Realized and unrealized gain (loss): | |||

| Net realized loss on investment transactions | (574,241 | ) | |

| Net change in unrealized appreciation (depreciation) on investments | 2,459,037 | ||

| Net realized and unrealized gain | 1,884,796 | ||

| Net increase in net assets resulting from operations | $ 2,077,721 | ||

| Six months ended

June 30, 2000 (Unaudited) |

Year ended

December 31, 1999 |

|||||

|---|---|---|---|---|---|---|

| Increase (Decrease) in Net Assets: | ||||||

| Operations: | ||||||

| Net investment income | $ 192,925 | $ 162,226 | ||||

| Net realized loss on investment transactions | (574,241 | ) | (626,497 | ) | ||

| Net change in unrealized appreciation (depreciation) on investments | 2,459,037 | 482,379 | ||||

| Net increase in net assets resulting from operations | 2,077,721 | 18,108 | ||||

| Distributions to shareholders: (Note 2) | ||||||

| From net investment income | - | (160,000 | ) | |||

| Net fund share transactions (Note 5) | 8,926,204 | 9,836,805 | ||||

| Total increase in net assets | 11,003,925 | 9,694,913 | ||||

| NET ASSETS: | ||||||

| Beginning of period | 20,137,097 | 10,442,184 | ||||

| End of period (including undistributed net investment income of $194,237 and $1,312, respectively) | $ 31,141,022 | $ 20,137,097 | ||||

| Six months

ended 6/30/00 (Unaudited) |

Year

ended 12/31/99 |

Period

ended 12/31/98† |

|||||||

|---|---|---|---|---|---|---|---|---|---|

| Net asset value, beginning of period | $ 8.34 | $ 8.49 | $ 10.00 | ||||||

| Income (loss) from investment operations: | |||||||||

| Net investment income | 0.06 | 0.07 | 0.03 | ||||||

| Net realized and unrealized gain (loss) on investments | 0.58 | (0.15 | ) | (1.51 | ) | ||||

| Total income (loss) from investment operations | 0.64 | (0.08 | ) | (1.48 | ) | ||||

| Less distributions to shareholders: | |||||||||

| From net investment income | - | (0.07 | ) | (0.03 | ) | ||||

| Net asset value, end of period | $ 8.98 | $ 8.34 | $ 8.49 | ||||||

| Total Return @ | 7.72% | ** | (1.04% | ) | (14.77% | )** | |||

| Ratios/Supplemental Data: | |||||||||

| Net assets, end of period (000’s) | $ 31,141 | $ 20,137 | $10,442 | ||||||

| Net expenses to average daily net assets: | |||||||||

| Before expense waiver | 0.88% | * | 1.07 | % | 0.85% | ** | |||

| After expense waiver | 0.76% | * | 0.75 | % | 0.44% | ** | |||

| Net investment income to average daily net assets | 1.56% | * | 1.13 | % | 0.42% | ** | |||

| Portfolio turnover rate | 38% | ** | 41 | % | 23% | ** | |||

*

|

Annualized

|

**

|

Percentage represents results for the period and are not annualized.

|

†

|

For the period from June 1, 1998 (commencement of operations) through December 31, 1998.

|

@

|

Total return information shown in the Financial Highlights tables does not reflect expenses that apply at the separate account level or to

related insurance products.

|

| Inclusion of these charges would reduce the total return figures for all periods shown.

|

| Number

of Shares |

Market Value |

|||

|---|---|---|---|---|

| EQUITIES - 86.9% | ||||

| Advertising - 1.9% | ||||

| Ackerley Group, Inc. | 11,700 | $ 137,475 | ||

| Harte Hanks Communications,

Inc. |

17,900 | 447,500 | ||

| 584,975 | ||||

| Automotive & Parts - 1.0% | ||||

| Dura Automotive Systems, Inc. * | 3,200 | 34,600 | ||

| Myers Industries, Inc. | 200 | 2,150 | ||

| United Auto Group, Inc. * | 30,700 | 280,137 | ||

| 316,887 | ||||

| Banking, Savings & Loans - 7.7% | ||||

| Banknorth Group, Inc. | 33,157 | 507,717 | ||

| CCB Financial Corporation | 3,000 | 111,000 | ||

| Commerce Bancorp, Inc. NJ | 13,100 | 602,600 | ||

| First Republic Bank * | 13,100 | 261,181 | ||

| Hudson City Bancorp, Inc. | 24,200 | 412,912 | ||

| Webster Financial Corporation | 22,080 | 489,900 | ||

| 2,385,310 | ||||

| Broadcasting, Publishing & Printing - 1.1% | ||||

| Houghton Mifflin Company | 100 | 4,669 | ||

| McClatchy Newspapers, Inc. | 10,500 | 347,812 | ||

| 352,481 | ||||

| Building Materials & Construction - 1.2% | ||||

| Elcor Corporation | 16,500 | 379,500 | ||

| Chemicals - 5.5% | ||||

| Olin Corp. | 44,200 | 729,300 | ||

| OM Group, Inc. | 11,700 | 514,800 | ||

| Spartech Corporation | 17,400 | 469,800 | ||

| 1,713,900 | ||||

| Commercial Services - 5.4% | ||||

| ABM Industries, Inc. | 20,700 | 476,100 | ||

| Advo, Inc. * | 27,500 | 1,155,000 | ||

| Landauer, Inc. | 3,800 | 59,137 | ||

| 1,690,237 | ||||

| Communications - 5.4% | ||||

| Ct Communications, Inc. | 25,700 | 730,844 | ||

| Inet Technologies, Inc. * | 7,400 | 401,450 | ||

| True North Communications, Inc. | 12,500 | 550,000 | ||

| 1,682,294 | ||||

| Number

of Shares |

Market Value |

|||

|---|---|---|---|---|

| Computers & Information - 2.0% | ||||

| Xircom, Inc. * | 13,400 | $636,500 | ||

| Containers - 0.8% | ||||

| U.S. Can Corporation * | 15,200 | 264,100 | ||

| Electric Utilities - 3.1% | ||||

| Calpine Corporation * | 7,700 | 506,275 | ||

| EL Paso Electric Co. * | 40,100 | 448,619 | ||

| 954,894 | ||||

| Electrical Equipment & Electronics - 13.4% | ||||

| Benchmark Electronics, Inc. * | 13,100 | 478,969 | ||

| Burr-Brown Corp. * | 6,100 | 528,794 | ||

| Cognex Corporation * | 12,400 | 641,700 | ||

| Cohu, Inc. | 15,700 | 423,410 | ||

| Dallas Semiconductor

Corporation |

17,000 | 692,750 | ||

| Lattice Semiconductor

Corporation * |

8,800 | 608,300 | ||

| Micrel, Inc. * | 15,500 | 673,281 | ||

| Teleflex, Incorporated | 3,100 | 114,894 | ||

| 4,162,098 | ||||

| Energy - 4.6% | ||||

| Newfield Exploration Company * | 11,800 | 461,675 | ||

| Precision Drilling Corporation | 16,400 | 633,450 | ||

| Stone Energy Corporation * | 5,700 | 340,575 | ||

| 1,435,700 | ||||

| Financial Services - 1.8% | ||||

| Eaton Vance Corp. | 12,100 | 559,625 | ||

| Foods - 2.6% | ||||

| International Home Foods, Inc. * | 17,700 | 370,594 | ||

| Morrison Management

Specialists, Inc. |

16,070 | 452,973 | ||

| 823,567 | ||||

| Healthcare - 1.8% | ||||

| Health Management Associates

Cl. A * |

42,500 | 555,156 | ||

| Industrial - Diversified - 2.0% | ||||

| Carlisle Cos., Inc. | 13,500 | 607,500 | ||

| Number

of Shares |

Market Value |

|||

|---|---|---|---|---|

| Insurance - 3.5% | ||||

| HCC Insurance Holdings | 22,000 | $ 415,250 | ||

| Highlands Insurance Group, Inc.* | 19,800 | 185,625 | ||

| White Mountains Insurance

Group, Inc. |

3,100 | 496,000 | ||

| 1,096,875 | ||||

| Machinery & Components - 5.8% | ||||

| Hardinge, Inc. | 17,350 | 181,091 | ||

| Helix Technology Corporation | 17,900 | 698,100 | ||

| Regal-Beloit Corporation | 19,100 | 306,794 | ||

| Roper Industries, Inc. | 21,300 | 545,813 | ||

| Tennant Co. | 1,600 | 60,000 | ||

| 1,791,798 | ||||

| Medical Supplies - 3.7% | ||||

| Bacou USA, Inc. * | 13,600 | 272,000 | ||

| Biomet, Inc. | 10,600 | 407,438 | ||

| Invacare Corporation | 17,500 | 459,375 | ||

| 1,138,813 | ||||

| Metals & Mining - 3.9% | ||||

| CompX International, Inc. | 18,800 | 381,875 | ||

| Matthews International Corp. | 15,200 | 440,800 | ||

| Reliance Steel & Aluminum

Company |

20,650 | 394,931 | ||

| 1,217,606 | ||||

| Miscellaneous - 0.6% | ||||

| Crossmann Communities, Inc. * | 11,500 | 189,750 | ||

| Pharmaceuticals - 1.9% | ||||

| Bindley Western Industries, Inc. | 22,033 | 582,497 | ||

| Real Estate - 1.0% | ||||

| Mid- Atlantic Realty Trust | 29,700 | 297,000 | ||

| Retail - 1.2% | ||||

| BJ’s Wholesale Club, Inc. * | 11,800 | 389,400 | ||

| Transportation - 4.0% | ||||

| C.H. Robinson Worldwide, Inc. | 16,300 | 806,850 | ||

| Hub Group, Inc. Cl. A * | 7,900 | 118,006 | ||

| M.S. Carriers, Inc. * | 18,400 | 324,300 | ||

| 1,249,156 | ||||

| TOTAL EQUITIES | ||||

| (Cost $25,235,638) | 27,057,619 | |||

| Principal

Amount |

Market Value |

|||||

|---|---|---|---|---|---|---|

| SHORT-TERM INVESTMENTS - 11.7% | ||||||

| Cash Equivalents - 3.4% | ||||||

| Bank of America Bank Note ** | ||||||

| 6.670% | 03/22/2001 | $ 22,819 | $ 22,819 | |||

| Bank of Montreal Bank Note ** | ||||||

| 6.630% | 08/16/2000 | 38,032 | 38,032 | |||

| Bank of Nova Scotia Eurodollar

Time Deposit ** |

||||||

| 7.000% | 07/03/2000 | 45,638 | 45,638 | |||

| Credit Agricole Bank Eurodollar

Time Deposit ** |

||||||

| 6.750% | 07/06/2000 | 152,128 | 152,128 | |||

| Credit Agricole Bank Eurodollar

Time Deposit ** |

||||||

| 6.750% | 07/07/2000 | 22,819 | 22,819 | |||

| Den Danske Bank Eurodollar

Time Deposit ** |

||||||

| 6.810% | 07/05/2000 | 83,670 | 83,670 | |||

| First Union Bank Note ** | ||||||

| 6.900% | 05/09/2001 | 22,819 | 22,819 | |||

| Fleet National Bank Eurodollar

Time Deposit ** |

||||||

| 7.260% | 10/31/2000 | 96,048 | 96,048 | |||

| HypoVereinsbank Eurodollar

Time Deposit ** |

||||||

| 6.750% | 07/05/2000 | 190,159 | 190,159 | |||

| Merrimac Money Market Fund ** | ||||||

| 6.440% | 07/03/2000 | 238,840 | 238,840 | |||

| Morgan Stanley Dean Witter & Co. ** | ||||||

| 6.890% | 07/17/2000 | 45,638 | 45,638 | |||

| Morgan Stanley Dean Witter & Co. ** | ||||||

| 6.910% | 11/22/2000 | 15,213 | 15,213 | |||

| Paribas Bank Eurodollar

Time Deposit ** |

||||||

| 6.750% | 07/05/2000 | 91,277 | 91,277 | |||

| 1,065,100 | ||||||

| Principal

Amount |

Market Value |

|||||||

|---|---|---|---|---|---|---|---|---|

| Repurchase Agreement - 8.3% | ||||||||

| Investors Bank & Trust Company Repurchase

Agreement, dated 06/30/00, |

||||||||

| 6.03%, due 07/03/00 (a) | $2,586,994 | $ 2,586,994 | ||||||

| TOTAL SHORT-TERM INVESTMENTS

(At Amortized Cost) |

3,652,094 | |||||||

| TOTAL INVESTMENTS - 98.6%

(Cost $28,887,732) *** |

$30,709,713 | |||||||

| Other Assets/(Liabilities) - 1.4% | 431,309 | |||||||

| NET ASSETS - 100.0% | $31,141,022 | |||||||

*

|

Non-income producing security.

|

**

|

Represents investment of security lending collateral. (Note 2).

|

***

|

Aggregate cost for Federal tax purposes. (Note 7).

|

(a)

|

Maturity value of $2,588,294. Collateralized by U.S. Government Agency obligation with a rate of 9.375%, maturity date of 09/25/2012, and

aggregate market value, including accrued interest, of $2,716,344.

|

| 1. The Fund | MML Small Cap Value Equity Fund (the “Fund”) is a diversified series of the MML Series

Investment Fund (“MML Trust”). The MML Trust is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as a no-load, registered open-end, management investment company. The MML Trust, which has eleven separate series of shares, is organized under the laws of the Commonwealth of Massachusetts as a Massachusetts business trust pursuant to an Agreement and Declaration of Trust dated December 19, 1984, as amended. On June 1, 1998, the Fund commenced operations. |

|

| The MML Trust was established by Massachusetts Mutual Life Insurance Company (“MassMutual”)

for the purpose of providing vehicles for the investment assets of various separate investment accounts established by MassMutual and by life insurance companies which are subsidiaries of MassMutual. Shares of the MML Trust are not offered to the general public. |

||

| 2. Significant

Accounting Policies |

The following is a summary of significant accounting policies followed consistently by the Fund in

the preparation of the financial statements in conformity with generally accepted accounting principles. The preparation of the financial statements in accordance with generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts and disclosures in the financial statements. Actual results could differ from those estimates. |

|

| Investment

Valuation |

Equity securities are valued on the basis of valuations furnished by a pricing service, authorized by

the Board of Trustees (“Trustees”), which provides the last reported sale price for securities listed on a national securities exchange or on the NASDAQ National Market System, or in the case of over- the-counter securities not so listed, the last reported bid price. Debt securities (other than short-term obligations with a remaining maturity of sixty days or less) are valued on the basis of valuations furnished by a pricing service, authorized by the Trustees, which determines valuations taking into account appropriate factors such as institutional-size trading in similar groups of securities, yield, quality, coupon rate, maturity, type of issue, trading characteristics and other market data. Money market obligations with a remaining maturity of sixty days or less are valued at either amortized cost or at original cost plus accrued interest, whichever approximates current market value. All other securities and other are valued at fair value in accordance with procedures approved by and determined in good faith by the Trustees, although the actual calculation may be done by others. |

|

| Portfolio securities traded on more than one national securities exchange are valued at the last price

on the business day as of which such value is being determined at the close of the exchange representing the principal market for such securities. All assets and liabilities expressed in foreign currencies will be converted into U.S. dollars at the mean between the buying and selling rates of such currencies against U.S. dollars last quoted by any major bank. If such quotations are not available, the rate of exchange will be determined in accordance with policies established by the Trustees. |

||

| Accounting for

Investments |

Investment transactions are accounted for on the trade date. Realized gains and losses on sales of

investments and unrealized appreciation and depreciation of investments are computed on the specific identification cost method. Interest income, adjusted for amortization of discounts and premiums on investments, is earned from the settlement date and is recorded on the accrual basis. Dividend income is recorded on the ex-dividend date. |

|

| Federal Income Tax | It is the Fund’s intent to continue to comply with the provisions of subchapter M of the Internal

Revenue Code of 1986, as amended (the “Code”), applicable to a regulated investment company. Under such provisions, the Fund will not be subject to federal income taxes on its ordinary income and net realized capital gains to the extent they are distributed or deemed to have been distributed to its shareholders. Therefore, no Federal income tax provision is required. |

|

| Dividends and

Distributions to Shareholders |

Dividends from net investment income and distributions of any net realized capital gains of the Fund

are declared and paid annually and at other times as may be required to satisfy tax or regulatory requirements. Distributions to shareholders are recorded on the ex-dividend date. Income and capital gain distributions are determined in accordance with income tax regulations which may differ from generally accepted accounting principles. These differences are primarily due to investments in forward contracts, passive foreign investment companies and the deferral of wash sale losses. As a result, net investment income and net realized gain on investment transactions for a reporting period may differ significantly from distributions during such period. Accordingly, the Fund may periodically make reclassifications among certain of its capital accounts without impacting the net asset value of the Fund. |

|

| Foreign Currency

Translation |

The books and records of the Fund are maintained in U.S. dollars. The market values of foreign

currencies, foreign securities and other assets and liabilities denominated in foreign currencies are translated into U.S. dollars at the mean of the buying and selling rates of such currencies against the U.S. dollar at the end of each business day. Purchases and sales of foreign securities and income and expense items are translated at the rates of exchange prevailing on the respective dates of such transactions. The Fund does not isolate that portion of the results of operations arising from changes in the exchange rates from that portion arising from changes in the market price of securities. |

|

| Net realized foreign currency gains and losses resulting from changes in exchange rates include

foreign currency gains and losses between trade date and settlement date on investment securities transactions, foreign currency transactions and the difference between the amounts of dividend recorded on the books of the Fund and the amount actually received. |

||

| Securities Lending | The Fund may make loans of portfolio securities; however, securities lending can not exceed 33% of

its total assets taken at current value. The loans are collateralized at all times with cash or securities with a market value at least equal to 100% of the market value of the securities on loan. As with other extensions of credit, the Fund may bear the risk of delay in recovery or even loss of rights in the collateral should the borrower of the securities fail financially. The Fund receives compensation for lending its securities. At June 30, 2000, the Fund loaned securities having a market value of $1,020,994, collateralized cash in the amount of $1,065,100, which was invested in short-term instruments. |

|

| Forward Foreign

Currency Contracts |

The Fund may enter into forward foreign currency contracts in order to convert foreign denominated

securities or obligations to U.S. dollar denominated investments. A forward foreign currency contract is an agreement between two parties to buy and sell a currency at a set price on a future date. The market value of a forward currency contract fluctuates with changes in forward foreign currency exchange rates. Forward foreign currency contracts are marked to market daily and the change in their value is recorded by the Fund as an unrealized gain or loss. When a forward foreign currency contract is extinguished, through delivery or offset by entering into another forward foreign currency contract, the Fund records a realized gain or loss equal to the difference between the value of the contract at the time it was opened and the value of the contract at the time it was extinguished or offset. |

|

| Forward foreign currency contracts involve a risk of loss from the potential inability of counterparties

to meet the terms of their contracts and from unanticipated movements in foreign currency values and interest rates. |

||

| The notional or contractual amounts of these instruments represent the investments the Fund has in

particular classes of financial instruments and do not necessarily represent the amounts potentially subject to risk. The measurement of the risk associated with these instruments is meaningful only when all related and offsetting transactions are considered. |

||

| There were no outstanding forward foreign currency contracts at June 30, 2000. | ||

| Forward

Commitments |

The Fund may purchase or sell securities on a “when issued,” delayed delivery or forward

commitment basis. The Fund uses forward commitments to manage interest rate exposure or as a temporary substitute for purchasing or selling particular debt securities. Delivery and payment for securities purchased on a forward commitment basis can take place a month or more after the date of the transaction. The Fund instructs the custodian to segregate assets in a separate account with a current market value at least equal to the amount of its forward purchase commitments. The price of the underlying security and the date when the securities will be delivered and paid for are fixed at the time the transaction is negotiated. The value of the forward commitment is determined by management using a commonly accepted pricing model and fluctuates based upon changes in the value of the underlying security and market repurchase rates. Such rates equate the counterparty’s cost to purchase and finance the underlying security to the earnings received on the security and forward delivery proceeds. The Fund records on a daily basis the unrealized appreciation/depreciation based upon changes in the value of the forward commitment. When a forward commitment contract is closed, the Fund records a realized gain or loss equal to the difference between the value of the contract at the time it was opened and the value of the contract at the time it was extinguished. Forward commitments involve a risk of loss if the value of the security to be purchased declines prior to the settlement date. The Fund could also be exposed to loss if it cannot close out its forward commitments because of an illiquid secondary market, or the inability of counterparties to perform. The Fund monitors exposure to ensure counterparties are creditworthy and concentration of exposure is minimized. At June 30, 2000, the Fund had no open forward commitments. |

|

| Financial Futures

Contracts |

The Fund may purchase or sell financial futures contracts and options on such futures contracts for

the purpose of hedging the market risk on existing securities or the intended purchase of securities. Futures contracts are contracts for delayed delivery of securities at a specific future date and at a specific price or yield. Upon entering into a contract, the Fund deposits and maintains as collateral such initial margin as required by the exchange on which the transaction is effected. Pursuant to the contract, the Fund agrees to receive from or pay to the broker an amount of cash equal to the daily fluctuation in value of the contract. Such receipts or payments are known as variation margin and are recorded by the Fund as unrealized gains or losses. When the contract is closed, the Fund records a realized gain or loss equal to the difference between the value of the contract at the time it was opened and the value at the time it was closed. At June 30, 2000, the Fund had no open financial futures contracts. |

|

| 3. Management

Fees and Other Transactions with Affiliates |

||

| Investment

Management Fee |

MassMutual provides all investment advisory, management and administrative services needed by the

Fund. For acting as such, MassMutual receives a monthly fee from the Fund at the annual rate of 0.65% of the first $100,000,000, 0.60% of the next $100,000,000, 0.55% of the next $300,000,000 and 0.50% of any excess over $500,000,000 of the average daily net asset value of the Fund. |

|

| MassMutual has entered into an investment sub-advisory agreement with David L. Babson and

Company, Inc. (“DLB”), pursuant to which DLB serves as the Fund’s sub-adviser providing day-to- day management of the Fund’s investments. DLB is a wholly-owned subsidiary of DLB Acquisition Corporation, which is a controlled subsidiary of MassMutual. MassMutual pays DLB a quarterly fee equal to an annual rate of 0.25% of the average daily net assets under management. |

||

| MassMutual has agreed, at least through April 30, 2001, to bear the expenses of the Fund to the

extent that the aggregate expenses (excluding the Fund’s management fee, interest, taxes, brokerage commissions and extraordinary expenses) incurred during the Fund’s fiscal year exceed 0.11% of the average daily net asset value of the Fund for such year. |

||

| Other | Certain officers and trustees of the Fund are also officers of MassMutual. The compensation of

unaffiliated directors of the Fund is borne by the Fund. |

| 4. Purchases and

Sales of Investments |

Cost of purchases and proceeds from sales of investment securities (excluding short-term

investments) for the six months ended June 30, 2000, were as follows: |

| Purchases | ||||

| Equities | $17,715,516 | |||

| Sales | ||||

| Equities | $ 7,184,342 |

| 5. Capital Share

Transactions |

The Fund is authorized to issue an unlimited number of shares, with no par value. The change in

shares outstanding for the Fund is as follows: |

| For the Six

months ended June 30, 2000 |

|||||

|---|---|---|---|---|---|

| Shares | |||||

| Reinvestment of dividends | 19,192 | ||||

| Sales of shares | 1,198,624 | ||||

| Redemptions of shares | (166,389 | ) | |||

| Net Increase | 1,051,427 | ||||

| Amount | |||||

| Reinvestment of dividends | $ 160,000 | ||||

| Sales of shares | 10,186,892 | ||||

| Redemptions of shares | (1,420,688 | ) | |||

| Net Increase | $ 8,926,204 | ||||

| For the Year ended

December 31, 1999 |

|||||

| Shares | |||||

| Reinvestment of dividends | 4,409 | ||||

| Sales of shares | 1,355,252 | ||||

| Redemptions of shares | (173,705 | ) | |||

| Net Increase | 1,185,956 | ||||

| Amount | |||||

| Reinvestment of dividends | $ 37,437 | ||||

| Sales of shares | 11,230,375 | ||||

| Redemptions of shares | (1,431,007 | ) | |||

| Net Increase | $ 9,836,805 | ||||

| 6. Foreign

Securities |

The Fund may also invest in foreign securities, subject to certain percentage restrictions. Investing in

securities of foreign companies and foreign governments involves special risks and considerations not typically associated with investing in securities issued by U.S. companies and the U.S. Government. These risks include revaluation of currencies and future adverse political and economic developments. Moreover, securities of many foreign companies and foreign governments and their markets may be less liquid and their prices more volatile than those of securities of comparable U.S. companies and the U.S. Government. |

| 7. Federal Income

Tax Information |

At June 30, 2000, the cost of securities and the unrealized appreciation (depreciation) in the value of

investments owned by the Fund, as computed on a Federal income tax basis, is as follows: |

| Federal

Income Tax Cost |

Tax Basis

Unrealized Appreciation |

Tax Basis

Unrealized Depreciation |

Net Unrealized

Appreciation |

|||||

|---|---|---|---|---|---|---|---|---|

| $28,887,732 | $3,505,759 | $1,683,778 | $1,821,981 |

| At December 31, 1999, the Fund had available, for Federal income tax purposes, unused capital

losses: |

| Amount |

Expiration Date |

|||

|---|---|---|---|---|

| $276,344 | December 31, 2006 | |||

| 626,497 | December 31, 2007 |

|

|